Business

Where Is India’s Battery?

Raghavan S Rao

Mar 14, 2026, 07:30 AM | Updated Mar 13, 2026, 04:16 PM IST

On August 26, 2025, a lithium-ion battery plant in Hansalpur, Gujarat, reached a milestone that had taken eight years to build. The TDSG facility — a joint venture between Suzuki Motor Corporation, Toshiba and Denso — began manufacturing electrodes for strong hybrid batteries, becoming the first plant in India to achieve electrode-level localisation in lithium-ion production. More than eighty per cent of the battery’s value was now created domestically. Over a million Maruti Suzuki vehicles already ran on batteries from this plant. By any measure, it was a serious industrial achievement.

On the same campus that day, the first units of Maruti Suzuki’s eVitara — Suzuki’s first battery electric vehicle — were dispatched for export. It should have been a day of uncomplicated celebration.

Instead, Maruti Suzuki’s chairman RC Bhargava chose to deliver a warning. Speaking to reporters at the event, he said that setting up a plant to manufacture cells for electric vehicles would cost roughly ₹20,000 crore. The raw materials, he noted, were controlled by a single supplier. “Risk is very high,” he said. “That is possibly one of the factors that is deterring people from making investments in battery cell manufacturing in India.” Nobody, he added, was making battery cells for electric vehicles in the country. People were packaging imported cells into battery packs, but actual cell production was not taking place.

The hybrid battery plant behind him proved that India could manufacture lithium-ion batteries. The eVitara being dispatched from the same campus proved that it would not do so for electric cars. The vehicle’s entire battery system — cells, pack, battery management system — was imported from BYD’s FinDreams subsidiary in China.

Three years earlier, on August 28, 2022, a foundation stone had been laid on the same Gujarat campus for a ₹7,300 crore plant to manufacture advanced chemistry cells for battery electric vehicles. That plant was supposed to produce the cells now arriving from Shenzhen. As of March 2026, it has not been built.

What happened between the two ceremonies — and what it reveals about why India can build hybrid batteries but not the cells its electric vehicles need — is the central question of India’s industrial ambitions in the decade ahead.

The word that conceals

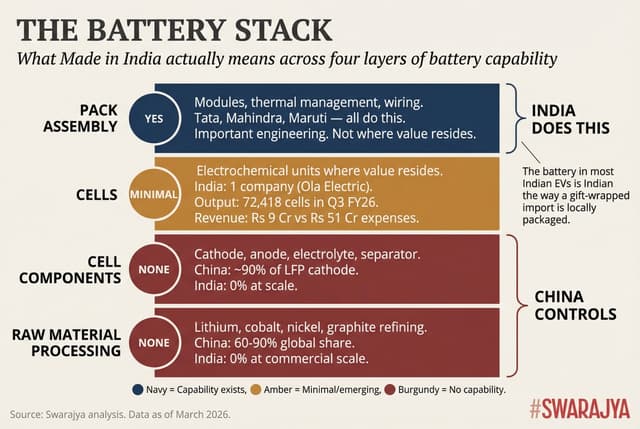

India’s electric vehicle industry uses the word “battery” to describe at least four distinct layers of technological capability. The conflation is not accidental. It allows announcements about “battery manufacturing” to sound more significant than they are.

At the base sits raw material processing: converting mined ores into battery-grade lithium carbonate, cobalt sulphate, nickel sulphate, and spherical graphite. China processes sixty to sixty-five per cent of the world’s lithium, over ninety per cent of its battery-grade graphite, and dominates cobalt and nickel refining. India processes none of these at commercial scale.

Above that sit cell components: cathode powder, anode material, electrolyte, and separator films. China produces roughly ninety per cent of the world’s lithium iron phosphate cathode material and holds a comparable share of graphite anode production. India manufactures none of these at scale.

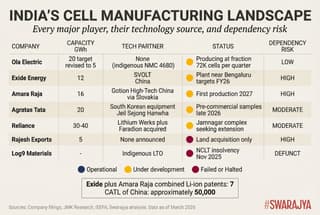

Above that sits the cell itself — the electrochemical unit where energy is stored, and where most of the value in a battery system resides. A cell requires precision coating of electrode slurries onto metal foils, calendering, cutting, stacking or winding, electrolyte filling, formation cycling, and aging. It is a chemical manufacturing process more akin to pharmaceutical production than automotive assembly. As of March 2026, exactly one company in India — Ola Electric — manufactures lithium-ion cells. Its output in the October–December 2025 quarter was 72,418 cells, generating revenue of ₹9 crore.

Above the cell sits pack assembly: arranging cells into modules with thermal management systems, structural housings, and wiring harnesses. This is what Tata Motors, Mahindra, and most Indian EV manufacturers do domestically. It is important engineering. It is not where the core intellectual property or the bulk of the value resides. Finally, the battery management system — the software that governs charging, discharging, thermal behaviour, and cell balancing — typically comes bundled with the cell maker’s proprietary technology. When Maruti imports BYD’s Blade battery pack, it imports the BMS with it. As Deepesh Rathore, founder of Insight EV, has noted, Chinese manufacturers closely guard their BMS intellectual property, particularly for lithium iron phosphate chemistry.

When Indian manufacturers or policymakers say “we are localising batteries,” they almost always mean pack assembly — the middle layer. The two layers where value and strategic control concentrate — cells below, BMS above — remain overwhelmingly foreign. The “battery” in most Indian electric vehicles is Indian the way a gift-wrapped import is locally packaged.

This hierarchy helps explain the paradox at Hansalpur. The TDSG hybrid battery plant succeeds because it operates at the upper layers of the stack, including electrode manufacturing, using Toshiba’s SCiB lithium titanate oxide chemistry. But LTO is a niche chemistry suited to hybrids — high power density, fast charging, but low energy density and expensive per kilowatt-hour. The mass electric vehicle market runs on lithium iron phosphate or nickel-manganese-cobalt chemistries, where China holds the commanding intellectual property position and BYD’s Blade technology sets the global benchmark. Bhargava’s remark that “nobody is making battery cells in India” was technically imprecise — his own joint venture plant makes them for hybrids. What he meant was that nobody is making the kind of cells that electric vehicles need. The dependency is chemistry-specific. And it is the chemistries that matter for the mass market where China’s grip is tightest.

The one factory that tried

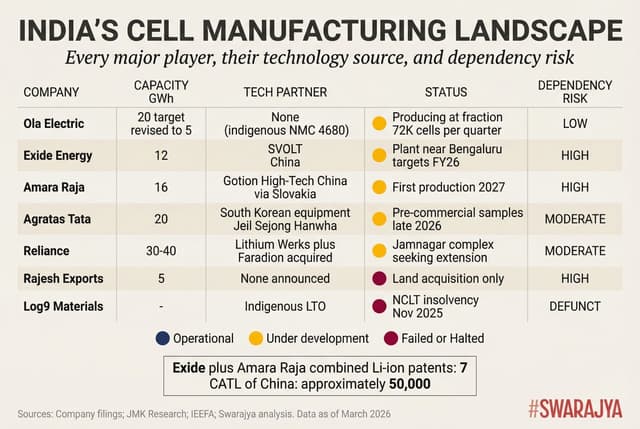

Ola Electric’s Gigafactory in Pochampalli, Krishnagiri district, Tamil Nadu, is the only facility in India that manufactures lithium-ion cells for electric vehicles. It deserves to be taken seriously. The plant produces 4680-format nickel-manganese-cobalt cylindrical cells — branded “Bharat Cell” — performing in-house electrode production, cell assembly, and formation. This makes Ola the first Indian company with complete cell-to-pack vertical integration.

The company has deliberately avoided Chinese technology partners. Its cathode materials come from Umicore of Belgium. Its anode materials come from Epsilon Advanced Materials, an Indian company. Its fast-charging research partnership is with StoreDot of Israel. Its manufacturing equipment is Korean. In an industry where every other Indian player has signed technology agreements with Chinese firms, Ola’s supply chain choices represent a conscious strategic bet — and the closest thing India has to a build-from-scratch approach.

The execution gap, however, is severe. Phase 1a was completed in May 2024 with 1.4 gigawatt-hours of installed capacity. Phase 1b, originally targeted for February 2025, remained incomplete as of early 2026. The plant’s installed capacity had reached approximately 2.5 GWh by December 2025, but actual production was a fraction of this — 72,418 cells in the October–December quarter, roughly 1.9 megawatt-hours. Cell revenue of ₹9 crore sat against ₹51 crore in cell operating expenses. The company’s original ambition of 20 GWh by 2026, announced at its Sankalp event in August 2024, has been abandoned. CEO Bhavish Aggarwal told analysts in February 2026 that 20 GWh was “not in the immediate roadmap,” pushing it to the second half of 2027 at the earliest.

The broader business provides uncomfortable context. Ola’s vehicle deliveries collapsed from over 125,000 units to roughly 32,700 in the same quarter — a sixty-one per cent year-on-year decline. Market share fell from nearly half the electric two-wheeler market in mid-2024 to roughly six per cent by January 2026. Revenue dropped over seventy per cent from its peak. The stock traded at approximately ₹25 in March 2026, down eighty-three per cent from its post-listing high and sixty-seven per cent below its IPO price. ICRA has downgraded both Ola Electric and its cell subsidiary. IFCI, the agency managing the government’s cell manufacturing incentive scheme, has issued notices for missed milestones, carrying penalties of ₹12.5 lakh per day.

India’s other indigenous cell hopeful, Log9 Materials, once celebrated for its lithium titanate fast-charging technology, was admitted into insolvency by the National Company Law Tribunal in November 2025 with debts exceeding ₹200 crore. The lesson is uncomfortable but unavoidable: building cells is considerably easier than building a viable business around them when competing against Chinese scale and cost advantages.

Fifty gigawatt-hours of ambition, 1.4 of reality

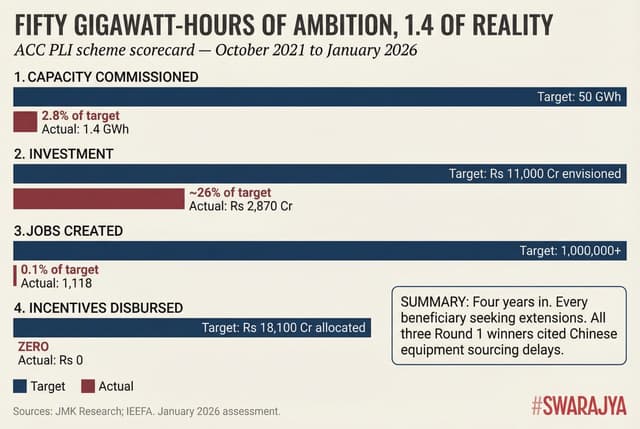

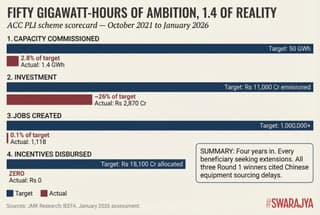

The government’s flagship effort to catalyse domestic cell manufacturing — the ₹18,100 crore Advanced Chemistry Cell Production Linked Incentive scheme, launched in October 2021 — was designed to create 50 GWh of capacity. A January 2026 assessment by JMK Research and the Institute for Energy Economics and Financial Analysis found that four years into the scheme, just 1.4 GWh had been commissioned. That is 2.8 per cent of the target. Zero incentives had been disbursed. Investments totalled approximately ₹2,870 crore — about a quarter of what was envisioned. Just 1,118 jobs had been created against a target of over one million.

The scheme’s current allocation stands at 40 GWh across three beneficiaries, with 10 GWh still untended. Ola Electric holds 20 GWh but is now targeting only 5 GWh by financial year 2029 — a dramatic scaling back. Reliance New Energy holds 15 GWh and is building at its Jamnagar complex, claiming on-time progress while simultaneously seeking a one-year extension for its first-round allocation. Rajesh Exports, a gold refiner with no battery experience, holds 5 GWh and has progressed only to land acquisition. All three Round 1 beneficiaries sought extensions in May 2025, citing delays in sourcing equipment from China.

Beyond the PLI scheme, several larger projects are under way — but each carries a dependency that the central question forces into view. Exide Energy Solutions is building a 12 GWh gigafactory near Bengaluru using technology licensed from SVOLT, a Great Wall Motors spinoff in China. The plant targets commercial production by the end of the current financial year. But Exide’s deep reliance on SVOLT for turnkey plant design makes it acutely vulnerable to China’s 2025 export controls on lithium iron phosphate cathode technology — the very chemistry Exide’s plant is designed to produce. Amara Raja is building a 16 GWh factory in Telangana with technology from Gotion High-Tech, routed through a Slovakian subsidiary. Its first production is expected in 2027. Together, India’s two largest battery companies hold seven patents related to lithium-ion technology. CATL of China holds approximately 50,000.

Agratas, the Tata Group’s battery arm, offers the most strategically considered approach. Its 20 GWh plant at Sanand, Gujarat, is deliberately sourcing South Korean manufacturing equipment — from Jeil M&S, Sejong Technology, Hanwha Momentum, and others — to avoid Chinese supply chain exposure. Pre-commercial samples are expected by late 2026. Reliance Industries, at its Jamnagar complex, plans 30 to 40 GWh of initial capacity using technology acquired from Lithium Werks and Faradion. But in January 2026, Bloomberg reported that Xiamen Hithium of China withdrew from technology-sharing talks with Reliance, citing Beijing’s export controls. China, it turned out, could veto India’s battery plans with a phone call.

The Budget 2026–27 response was telling. The ACC PLI allocation was cut by 44.5 per cent, while a new ₹22,919 crore Component Manufacturing Scheme was approved covering lithium-ion cells among other products. Import duties on lithium compounds were zeroed out. Duties on finished battery packs were raised to twenty per cent. The government was, in effect, acknowledging the first scheme’s failure while trying to create a tariff gradient favouring domestic manufacturing. Whether a tariff gradient works without the underlying capability is the question the budget could not answer.

Three waves

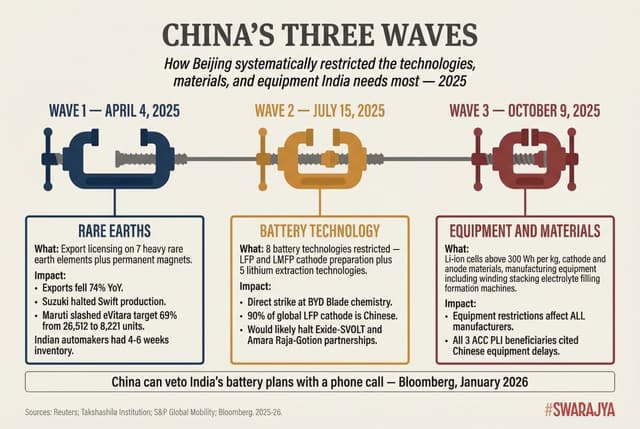

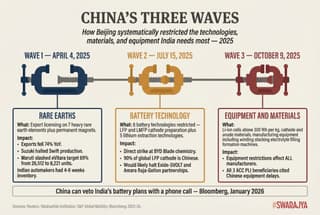

The context in which Indian companies are attempting to build cell manufacturing is not static. It is actively deteriorating. China deployed a cascading series of export restrictions through 2025 that systematically targeted the technologies, materials, and equipment India needs most.

On April 4, 2025, Beijing imposed export licensing requirements on seven heavy rare earth elements and permanent magnet materials — a retaliatory measure following US tariffs. The mechanism was not an outright ban but a case-by-case licensing process taking approximately forty-five days per application. The impact was immediate. China’s rare earth magnet exports fell seventy-four per cent year-on-year in May. Suzuki Motor halted Swift production at its Sagara plant in Japan. Indian automakers had only four to six weeks of inventory, with SIAM warning that production could halt entirely.

On June 10, Reuters reported, citing an internal Maruti Suzuki document, that the company had slashed its eVitara production target for April–September 2025 by sixty-nine per cent — from 26,512 units to 8,221 — because of rare earth supply constraints. One day before the Reuters story, Bhargava had told PTI there was “no impact” on production. Two days later, a Maruti spokesperson stated there was “no disruption.” The gap between the public denials and the internal production cut captures, more precisely than any policy document could, how India’s automobile industry talks about its China dependency: publicly minimising what it privately manages as a crisis.

On July 15, China restricted exports of eight battery technologies, including lithium iron phosphate and lithium manganese iron phosphate cathode material preparation technology, along with five lithium extraction and processing technologies. The scope was broader than an initial January draft, capturing what analysts described as third- and fourth-generation LFP technologies. Chinese companies produce approximately ninety per cent of global LFP cathode materials. This was a direct strike at the chemistry underpinning BYD’s Blade battery — the very technology in the Maruti eVitara.

On October 9, controls broadened further to physical products and equipment: lithium-ion cells above 300 Wh/kg energy density, cathode and anode materials, and critically, manufacturing equipment including winding machines, stacking machines, electrolyte filling machines, and formation systems. While mainstream EV battery cells fall below the cell energy density threshold, the equipment restrictions affect all manufacturers. The Takshashila Institution assessed that the July restrictions would “likely halt” technology partnerships of the kind Exide has with SVOLT and Amara Raja has with Gotion. All three ACC PLI beneficiaries cited Chinese equipment sourcing delays when requesting deadline extensions.

The Indian government’s response to the rare earth crisis included a ₹7,280 crore scheme for domestic rare earth permanent magnet manufacturing and dedicated Rare Earth Corridors across Odisha, Kerala, Andhra Pradesh, and Tamil Nadu, announced in Budget 2026–27. These are significant commitments. S&P Global Mobility cautioned in March 2026 that building automotive-grade rare earth supply chains “will take years.”

Forty years of renting, now in a different currency

Maruti Suzuki’s decision to import BYD’s Blade battery system for its first electric vehicle would be less significant if it were an exception. It is not. It is the latest iteration of a pattern that has defined India’s automobile industry for its entire modern history.

In more than four decades as India’s largest carmaker, Maruti Suzuki has never designed a single engine. Every powerplant is engineered by Suzuki Motor Corporation in Hamamatsu and manufactured in India. Over the five years to FY2015, Maruti paid roughly ₹11,870 crore in royalties to Suzuki against pre-tax profits of ₹16,770 crore — meaning up to forty-six per cent of earnings were remitted to its parent as payment for technology the Indian company was never permitted to develop itself. The proxy advisory firm IiAS described these payouts as “extortive.” In FY2013, Maruti’s royalty payments equalled 102 per cent of Suzuki Motor Corporation’s standalone profit. The Indian subsidiary was, in effect, funding its parent’s entire operation.

The EV transition was supposed to break this cycle. When the foundation stone was laid in August 2022 for BEV battery manufacturing at Gujarat, the implication was that Maruti would manufacture the core technology of its electric future domestically. Instead, the foundation stone became an import contract. The geography of dependency shifted from Hamamatsu to Shenzhen. The architecture — Indian capital, Indian labour, Indian market access exchanged for foreign core technology — remained identical.

The pattern extends well beyond Maruti. Tata Motors’ Revotron engine, presented in 2014 as India’s first indigenous turbocharged petrol powerplant, was optimised by AVL of Austria, with Bosch supplying the engine control unit and Honeywell the turbocharger. Its flagship SUVs still run on a Fiat-designed diesel. Mahindra’s electric vehicles use BYD cells, a Valeo powertrain integrating motor, inverter, and transmission, Bosch vehicle control, and Mobileye driver assistance. What Mahindra engineers in-house — the platform architecture, pack assembly, thermal management — is meaningful integration work. But the company’s contribution to the core EV powertrain, the parts that actually make the car move, is zero.

Across automobiles, electronics, batteries, and pharmaceuticals, Indian companies have spent the years since 2020 signing joint ventures, licensing agreements, and technology partnerships with Chinese firms at extraordinary pace. The deals differ in structure and sector. They share a common architecture: Indian capital and market access exchanged for Chinese technology. And in sector after sector, a common outcome is emerging. India is building factories. It is not, in any meaningful sense, building capability.

The comparison that stings most is with companies that started from comparable positions and chose differently. In 2010, Geely of China was ranked dead last in J.D. Power’s quality survey. Its cars scored near-zero on crash tests. Toyota had sued it for copying its logo. Over the following decade, Geely invested $11 billion in learning from its Volvo acquisition, establishing joint R&D centres where Chinese and Swedish engineers co-developed vehicle platforms. By 2020, Geely had independently designed the SEA electric vehicle architecture. Volvo’s own EX30 now rides on Geely’s platform. The technology flow reversed entirely. In March 2021, Xiaomi announced it would build electric cars with no automotive experience, no car patents, no factory. It pledged $10 billion, built from scratch, and by February 2026 had delivered over 600,000 vehicles on self-designed platforms with more than 1,200 automotive patents filed.

Hyundai’s Alpha engine project offers the most directly relevant precedent. In 1983, engineer Lee Hyun-soon launched a programme to design Korea’s first indigenous engine. Mitsubishi’s chairman reportedly dismissed the attempt as doomed. After 156 design corrections in a single year, testing in Arizona deserts and Canadian winters, and roughly 100 billion won in investment over seven years, the Alpha debuted in 1991. By 2004, Mitsubishi was paying royalties to Hyundai. The student had become the teacher in barely two decades. No Indian automotive company has yet reached the stage where a former technology supplier pays it royalties.

Two foundation stones, one question

The TDSG hybrid battery plant at Hansalpur represents what is possible when conditions align: a deep partnership begun in 2017, a Japanese technology partner willing to transfer electrode-level know-how, a niche chemistry where the intellectual property was available for sharing, and eight years of patient execution. More than a million vehicles. Eighty per cent domestic value. It works.

The empty plot next to it, where the BEV battery plant was supposed to rise, represents the far harder problem. For lithium iron phosphate and nickel-manganese-cobalt chemistries — the chemistries that will power the mass electric vehicle market — the intellectual property holders are Chinese. And China is now actively restricting transfer. India missed the window to build these partnerships before geopolitics closed the door. The Budget 2026–27 measures — zero duties on lithium compounds, Rare Earth Corridors, critical mineral missions — are pragmatic and necessary. They are also, unmistakably, management of a dependency rather than escape from it.

Escape would require something India has not yet attempted: sustained R&D investment beyond the current 0.64 per cent of GDP, mandatory indigenisation clauses attached to every partnership receiving government approval or subsidies, and a unified economic security institution with the authority to negotiate technology absorption as a national strategy. India spends $76 billion annually on R&D. China spends $786 billion. Geely alone invested more in learning from Volvo than India’s entire battery PLI allocation.

The question “Where is India’s battery?” has a precise answer in 2026, and the precision is what makes it uncomfortable. For hybrids, the battery is in Gujarat, manufactured with Japanese technology, and it works. For electric cars, the battery is in Shenzhen, manufactured by BYD, a company India rejected as an equity partner on national security grounds in 2023 but now imports from at scale. For the government’s cell manufacturing scheme, the battery exists mostly on paper — 2.8 per cent of target, zero incentives disbursed, every beneficiary seeking deadline extensions.

Bhargava said at Hansalpur that Indian scientists “have the capability to create their own solutions.” He invoked the vision of self-sufficiency. He is probably right. But his company’s answer to the ₹20,000 crore question — the question of whether to invest in building genuine cell chemistry capability from first principles or to import the finished product from China — was to let BYD answer it instead.

Somewhere in Tamil Nadu, Ola Electric’s Gigafactory produces cells at a pace that would take centuries to match a single year of CATL’s output. Somewhere in Aurangabad, JSW’s 630-acre automotive site rises on platforms designed in Shanghai. Somewhere in Bengaluru, Exide waits for SVOLT technology that China’s export controls may no longer permit to arrive. And in Gujarat, two foundation stones sit side by side — one marking a factory that produces batteries, the other marking a factory that was supposed to produce the batteries that matter. The distance between them is not measured in metres. It is measured in the choices India has not yet made.

A public policy consultant and student of economics.