Defence

Six Flaws That Could Sink India's New Defence Procurement Code Before It Launches

Swarajya Staff

Feb 20, 2026, 05:09 PM | Updated 05:31 PM IST

India's draft Defence Acquisition Procedure 2026 is, on paper, the most ambitious overhaul of military procurement the country has attempted.

The philosophical shift from "Made in India" to "Owned by India," the formalisation of Indigenous Design as a testable construct, the recognition that AI and software-first systems need fundamentally different procurement timelines.

All of this is directionally excellent. After Operation Sindoor proved that Indian-built systems perform when the stakes are existential, DAP-2026 has the rare opportunity to codify a wartime lesson into peacetime policy.

But the draft, as it stands, contains structural loopholes that risk turning this opportunity into a quiet subsidy for trading companies at the expense of the very innovators the policy claims to champion. The problems are not in the intent — the intent is sound.

They are in the implementation architecture, where imprecise definitions and weak enforcement mechanisms create perverse incentives that rational market actors will inevitably exploit. Here are the fault lines that need urgent repair.

The Trader vs. Innovator Problem

The most dangerous provision in DAP-2026 is one that sounds perfectly reasonable on the surface. Acquired intellectual property qualifies for Indigenous Design status, provided complete rights are transferred to an Indian-owned entity. The intent is pragmatic. It would enable technology absorption, but the effect is catastrophic for genuine innovators.

IDDM stands for Indigenously Designed, Developed and Manufactured. Each word is supposed to carry meaning. A company that purchases complete IP from a foreign OEM has not designed anything. The design was done abroad. It has not developed anything. The development was done abroad.

It has, at best, manufactured using someone else's blueprint. What the draft actually permits is a category that has no place in the IDDM framework: Foreign Designed, Foreign Developed, Indian Purchased.

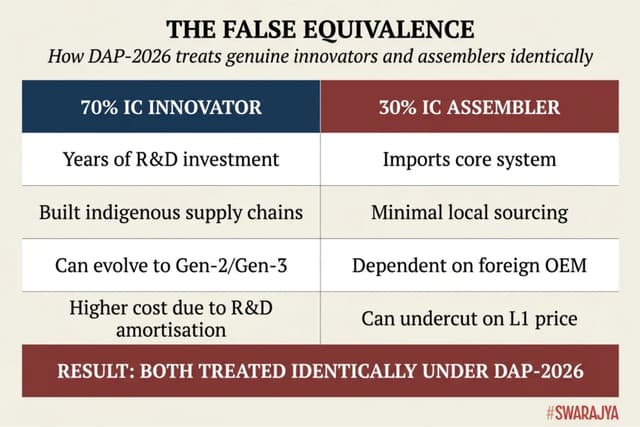

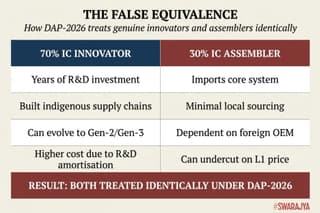

Consider the economics. A company that has spent years building an advanced electronic warfare system or an AI-based target recognition platform carries the full burden of R&D amortisation. A trading company that purchases equivalent IP from a foreign OEM carries none of that burden. Under DAP-2026, both receive identical IDDM classification.

When the two compete on price, as the L1 framework demands, the trader wins every time. The innovator, having invested in actual capability, is punished for the investment.

But the strategic damage runs deeper than unfair competition. Purchased IP has a shelf life of five to seven years before obsolescence, and in the age of AI, that window is shrinking fast. The company that bought the IP cannot upgrade it because it never built the engineering team that created it.

When the next generation is needed, it returns to the same foreign OEM, hat in hand, at whatever price the OEM chooses to set. India's "self-reliance" becomes a perpetual licence-to-buy, not a genuine indigenous capability.

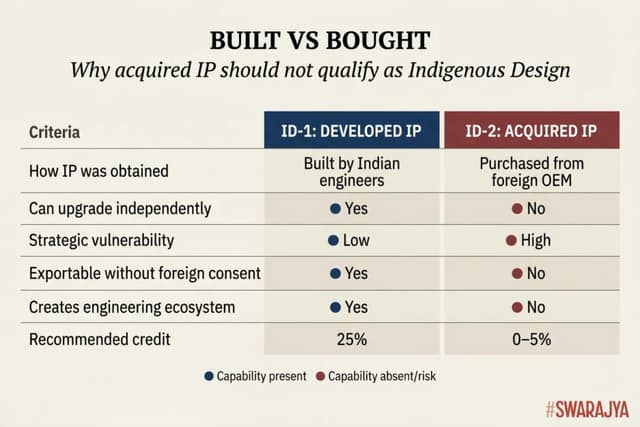

The fix requires creating two distinct categories. ID-1, for Developed IP, should cover technology conceived, designed, and iterated in India by Indian engineering teams, evidenced by design history files, version control records, patents filed from India, and demonstrated ability to modify the system without foreign assistance.

ID-2, for Acquired IP, should cover technology purchased or transferred from abroad, with the acquiring company required to demonstrate a credible absorption roadmap with enforceable milestones.

ID-1 should receive full evaluation credit. ID-2 should receive partial credit at best, with no eligibility for direct order placement.

Moreover, where a foreign OEM sells IP into a domain where an Indian company has demonstrably developed competing technology, evidenced by patents, DRDO trial participation, or iDEX involvement, the acquisition should trigger a mandatory review to determine whether it constitutes genuine technology transfer or a competitive countermove to undercut the domestic innovator.

An Invitation to Cheat

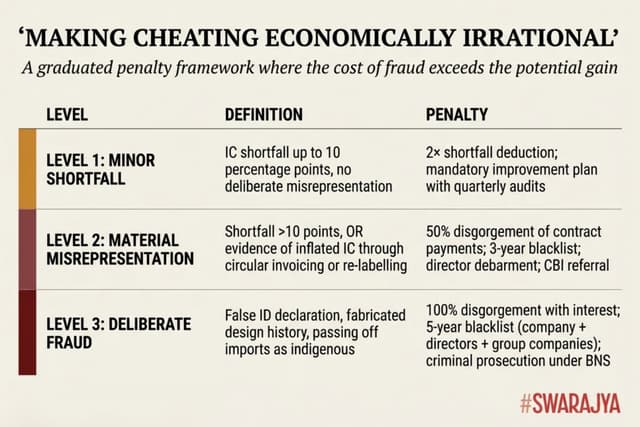

If the trader-versus-innovator problem is DAP-2026's most dangerous provision, the penalty framework is its most negligent.

Under the current draft, the consequence for false or inflated Indigenous Content or Indigenous Design claims is essentially a proportionate deduction from payments, roughly five per cent of the base contract price, plus forfeiture of the performance-cum-warranty bank guarantee. That is not a deterrent. It is a business calculation.

A company that falsely claims IDDM status to win a Rs 500 crore contract risks losing Rs 25–50 crore if caught. But it has captured the order, displaced a genuine innovator, and established itself as the incumbent for follow-on contracts worth multiples of the original.

The expected value of cheating massively exceeds the expected cost of getting caught. Any rational economic actor will choose to cheat.

The comparison with other domains is instructive.

Under India's securities law, market fraud attracts disgorgement of profits plus penalties up to three times the gain. Under the US False Claims Act, defence procurement fraud triggers treble damages plus per-claim penalties, criminal prosecution carrying up to twenty years' imprisonment, and debarment of both the company and its responsible individuals. DAP-2026's five per cent deduction is, by any comparative standard, the weakest penalty regime of any comparable domain.

What is needed is a graduated framework that makes cheating economically irrational. Minor shortfalls, where actual IC falls short of declared IC by up to ten percentage points without evidence of deliberate misrepresentation, should attract a deduction of twice the shortfall value, plus mandatory quarterly audits.

Material misrepresentation, with shortfalls exceeding ten points, or evidence of inflated IC through circular invoicing and re-labelling, should trigger disgorgement of fifty per cent of total contract payments, a three-year blacklist from defence procurement, and personal debarment of the directors who signed the declarations.

Deliberate fraud, fabricating design history files, passing off imported systems as indigenously designed, should attract full disgorgement with interest, five-year blacklisting of the company and all group entities, and mandatory criminal prosecution under applicable provisions of the Bharatiya Nyaya Sanhita.

Critically, debarment must extend to all entities under common ownership or control. The practice of fraudulent companies reconstituting under a different name to circumvent blacklisting is well-documented and must be closed off. And IC/ID self-certification must be signed personally by the CMD/CEO and CTO under penalty of perjury.

If a chartered accountant faces criminal prosecution for signing a false audit report, a director who signs a false IDDM declaration in a defence contract, a matter of national security, must face at least equivalent consequences.

Treating Assemblers and Innovators as Equals

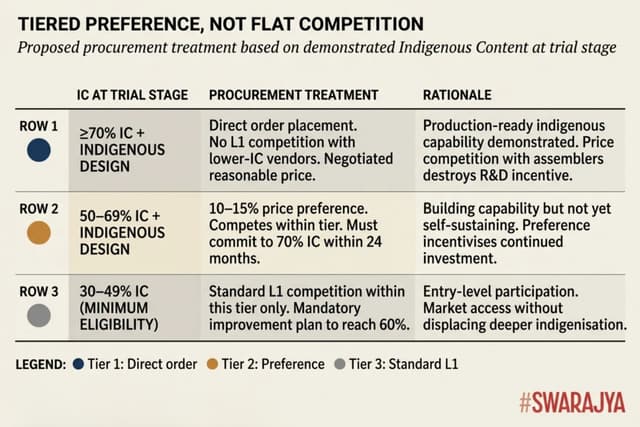

DAP-2026 requires only 30 per cent Indigenous Content at the prototype or demonstration stage for Buy (Indian-IDDM), with 60 per cent required overall. The 30 per cent threshold is intended as a minimum entry barrier.

The problem is that it functions as the only barrier. A company demonstrating 70 per cent IC at trials is treated identically to one demonstrating 30 per cent. Both qualify. Both proceed. Both compete on L1 price.

The economics are brutal for the innovator. Building indigenous supply chains costs more than importing and assembling. A company at 30 per cent IC can undercut one at 70 per cent IC on price, winning the order despite contributing far less to national capability.

If the only reward for achieving deep indigenisation is higher costs and no competitive advantage, the rational business decision is to stop investing in R&D and settle for assembly.

The 30 per cent floor should remain as it enables new entrants, but the draft needs a tiered preference mechanism above it.

A vendor demonstrating 70 per cent or greater IC with Indigenous Design at trial should receive direct order placement on a negotiated reasonable price basis, without L1 competition against lower-IC vendors. Between 50 and 69 per cent, a price preference of 10–15 per cent over lower-IC vendors would incentivise continued investment while maintaining competitive pressure.

The existing 15 per cent ID credit is directionally correct but structurally weak. It should be increased to 20–25 per cent for genuinely developed IP, and eliminated entirely for acquired IP.

Moreover, IC claims at trial must be verified by independent third-party audit, not self-certification. Self-certification without strong verification is an invitation to the gaming that the penalty framework is currently too weak to deter.

Software, AI, and the Hardware Hangover

DAP-2026 recognises that AI, quantum, and software-intensive systems need special procurement protocols. But the IC/ID framework remains fundamentally hardware-oriented, which is a problem when software represents 60–80 per cent of the value in modern defence systems and over 90 per cent of the competitive differentiation. A simulator, a counter-drone system, an EW suite, or an AI-based target recognition platform is primarily software.

The fix requires treating software IC/ID separately and with higher evaluation weight for software-intensive systems. No system should qualify as IDDM unless the complete source code is owned by the Indian entity, resides in India, and can be modified without foreign assistance. Access to compiled code or API access is not ownership.

Trained AI/ML models, training datasets, and the algorithms that produce them should be explicitly recognised as protectable IP. A company that has trained a model on Indian operational data has created something a foreign OEM cannot replicate.

This connects directly to the trial reform question. DAP-2026's recognition that traditional two-to-three-year Field Evaluation Trials are incompatible with fast-evolving technologies is welcome, and its proposal for simulation-based evaluation is sensible in principle. But the implementation must be precise.

What gets simulated is the threat environment, never the equipment itself. The equipment under test must always be real, physical hardware, connected to government-controlled simulated environments that present realistic threats and test the system's actual sensors, processors, and effectors in real time.

A company that shows up with a software demo instead of functioning hardware should be shown the door. The US Army has operated Hardware-in-the-Loop testing facilities at Redstone Arsenal for over four decades. The principle they validate is the one India should adopt. Simulation extends the test envelope and compresses timelines, but it never substitutes for demonstrated hardware performance.

Ownership Beyond Shareholding

DAP-2026 hard-codes the requirement for greater than 50 per cent Indian citizen ownership and no more than 49 per cent FDI. This is necessary but insufficient, because the real question is not who owns the shares but who controls the technology decisions.

Several Indian companies with majority Indian shareholding are effectively controlled by their foreign technology partners through licence agreements that give the foreign partner veto over product modifications, non-compete clauses that prevent the Indian company from developing competing technology, and key-man dependencies where all critical engineering decisions are made by foreign nationals on deputation.

The ownership test must extend to technology decision authority. The CTO must be an Indian citizen with actual decision-making power. It must require that at least 75 per cent of engineering headcount be Indian citizens based in India. It must prohibit restrictive covenants that prevent the Indian entity from competing freely in domestic and export markets. Without these provisions, the shareholding test becomes a fig leaf over continued foreign control.

Bridging the Valley of Death

The integration of iDEX, TDF, and Make-I/II into a unified Development Scheme with IDDM as the procurement output is excellent architecture. The Low Cost Capital Acquisition (LCCA) construct, allowing Services to quickly exploit proven Indian technologies for up to Rs 75 crore per case, is a genuinely innovative mechanism. But the transition from successful prototype to production order remains where Indian innovators go to die.

If a Make-II or iDEX prototype successfully completes trials, the procuring Service should be mandated to place an initial order within six months. "Successful trial but no order" should require written justification from the Service Chief, not the vendor.

LCCA cases should carry a mandatory, time-bound pathway to bulk procurement, within twelve months of delivery, with a designated officer accountable for the transition and a formal feedback loop where operational experience shapes the SQR for bulk procurement. The five-year, ten-times window for follow-on orders without re-tendering is a strong provision that must be strictly enforced. any attempt to create a competing RFP during this window should require DAC-level justification.

India has arrived at a genuine inflection point. The question DAP-2026 must answer is whether India wants to be a buyer of defence technology or a builder of it. Every provision in the procedure should be stress-tested against this question. Where a provision inadvertently rewards buying over building, it should be amended.