Economy

Can Gas Tankers Help India Realise Its Shipbuilding Revolution?

Ankit Saxena

Feb 19, 2026, 01:27 PM | Updated Feb 23, 2026, 07:52 PM IST

India pays approximately $75 billion annually to charter foreign vessels for its trade. Nearly 95 per cent of the country's trade by volume and 70 per cent by value moves through maritime routes, yet Indian shipyards account for less than 1 per cent of global output.

This equation might see some changes now. Recently, India's Shipping Corporation has issued a tender that doubles as industrial policy.

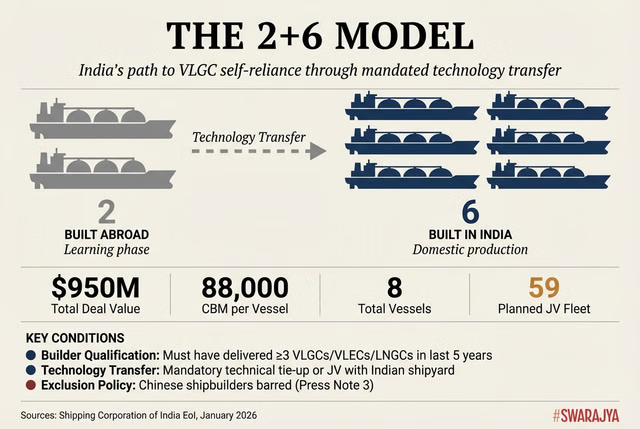

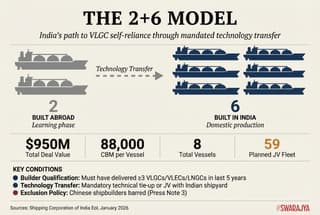

SCI has issued an Expression of Interest (EoI) for the construction of eight Very Large Gas Carriers (VLGCs) valued at approximately $950 million.

The structure of the tender is designed such that two of the vessels are permitted to be constructed at an international shipyard with a proven track record, defined as having delivered at least three VLGCs, Very Large Ethane Carriers (VLECs), or Liquefied Natural Gas Carriers (LNGCs) within the last five years. The remaining six must be built domestically.

Historically, India has been a major consumer rather than a provider of these shipping services. Until now, it has not built VLGCs domestically and relies on other countries for such shipments.

In recent years, the global energy transition has placed a significant premium on the maritime transportation of liquefied gases, specifically Liquefied Petroleum Gas (LPG) and Liquefied Natural Gas (LNG).

As India manoeuvres toward becoming a $5 trillion economy, its dependence on energy imports has underscored a critical strategic vulnerability: the lack of a robust domestic fleet of Very Large Gas Carriers.

The Mechanics of the EoI

To participate, the winning international shipbuilder is required to enter into a technical tie-up, joint venture, or strategic alliance with an Indian shipyard, effectively mandating a transfer of high-end maritime technology.

This procurement is being managed on behalf of a proposed joint venture led by SCI, which will hold a 50 per cent stake, alongside major state-owned energy firms like Indian Oil Corporation (IOCL), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL).

This EoI can thus be seen as a calculated effort to leverage India's massive energy demand to force a transfer of high-end technology from established maritime giants in South Korea and Japan to domestic soil.

By mandating that six of the eight vessels be built in Indian shipyards through technical tie-ups, SCI is creating a pathway for Indian shipbuilders to enter the elite tier of gas carrier construction—a segment historically dominated by a handful of East Asian yards.

What Are VLGCs?

To understand the strategic importance of this EoI, one must consider the technical nature of VLGCs and India's broader energy trajectory.

A Very Large Gas Carrier is a highly specialised vessel, typically defined by a capacity exceeding 80,000 cubic metres (cbm), designed for the transoceanic transport of liquefied petroleum gas (LPG), propane, and butane. The SCI tender specifies 88,000 cbm vessels—ships approximately 230 metres long and 38 metres wide that must maintain volatile gases in liquid state through cryogenic cooling at temperatures approaching minus 50 degrees Celsius.

These are, in essence, floating pipelines requiring precision engineering in metallurgy, insulation, and cargo containment systems. The technical barriers to entry explain why only a handful of shipyards globally possess the capability to build them.

India's interest in these vessels stems from its position as the world's second-largest LPG consumer. The country imports approximately 67 per cent of its LPG requirements, with demand continuing to grow. This import dependence is currently serviced almost entirely by foreign-flagged vessels.

In recognition of India's massive energy demand and the need to reduce shipping dependency, two VLGCs were commissioned for India's self-reliance in larger carrying shipments only last year. However, these were built in South Korea.

Induction of Sahyadri and Shivalik

In 2025, India inducted two VLGCs, Sahyadri and Shivalik, into the SCI fleet. Sahyadri was inducted on 14 August 2025, followed by Shivalik on 10 September 2025.

These 225-metre-long carriers, built in South Korea, each possess a capacity of 82,000 cbm and are dual-classed with DNV and the Indian Register of Shipping (IRS).

The maiden voyage of Shivalik carried 46,000 metric tonnes of LPG from Ruwais, UAE, to Visakhapatnam for IOCL. This demonstrated the operational capacity of Indian crews and managers to handle advanced gas assets. However, the carriers were built in South Korea.

The East Asian Stronghold

The market for gas carriers is currently concentrated in South Korea, Japan, and China.

In 2025, South Korean shipbuilders like HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean held a 22 per cent share of the global order book by Compensated Gross Tons (CGT), particularly in the high-value LNG and LPG segments.

The secret to Korea's success is the "integrated ecosystem" in Ulsan, where shipyards are surrounded by hundreds of Tier II and III suppliers, ensuring just-in-time delivery of everything from engines to tiny valves.

Yards like HD Hyundai and Samsung Heavy Industries lead the world in LNG and VLGC orders. HD Korea Shipbuilding & Offshore Engineering, for instance, secured 129 ship orders in 2025 alone, valued at over $18 billion. Korean yards dominate approximately 70 per cent of the global LNG carrier market.

China commands the largest market share by volume—over 56 per cent of global shipbuilding output in 2025—built on government subsidies, competitive steel, and massive scale.

Beijing is now pivoting from bulk carriers toward high-value vessels, capturing 78.5 per cent of global alternative fuel vessel orders in 2024.

Japan holds approximately 5 per cent of the global order book by new orders and is known for environmentally advanced designs.

Japanese shipbuilders like Imabari lead in ammonia-ready and hydrogen propulsion technologies. Much of Japan's order book is focused on bulk carriers and specialised LPG and LNG ships.

What India Needs to Build This Ecosystem

For India to successfully transition from building standard tankers to VLGCs, it must bridge substantial gaps in its industrial ecosystem.

The construction of gas carriers requires advanced metallurgy, specifically high-nickel and cryogenic steels capable of maintaining toughness at extreme sub-zero temperatures.

While Indian steel majors like SAIL, Tata Steel, and JSW are expanding their high-grade capacities, the ancillary supply chain for specialised components such as reliquefaction units and boil-off gas (BOG) management systems remains nascent.

Furthermore, the industry requires a highly specialised workforce. A single investment in shipbuilding is estimated to boost associated jobs by 6.4 times, yet the current shortage of skilled labour in cryogenic welding and naval architecture presents a hurdle.

Third is the question of port infrastructure. There are currently 61 shipyards in India, but the capability for "mega-shipbuilding" is concentrated among limited hubs.

Cochin Shipyard Limited (CSL) has recently inaugurated a ₹1,799 crore new dry dock, at 310 metres long and 75/60 metres wide. This "stepped" dock is designed specifically for specialised vessels like LNG and LPG carriers and is equipped with a 600-tonne gantry crane sourced from South Korea's Hyundai Samho.

CSL is notably the first Indian yard to obtain a licence from GTT (France) to utilise its membrane-type technology for cryogenic tanks.

The L&T Kattupalli facility near Chennai spans 1,250 acres and features a 21,050-tonne capacity shiplift and transfer system.

The yard's 16-metre channel depth and integrated design centre provide the necessary scale for the construction and outfitting of large-scale commercial and defence vessels.

The tender also sits within a broader policy framework designed to create the conditions for shipbuilding at scale.

The Shipbuilding Financial Assistance Scheme, with a corpus of Rs 24,736 crore, provides graded financial assistance of 15 to 25 per cent of vessel contract value, with the highest incentives reserved for specialised and green vessels. The Shipbuilding Development Scheme, with an outlay of Rs 19,989 crore, supports capacity augmentation, 100 per cent capital support for common infrastructure in greenfield clusters, 25 per cent for brownfield expansion.

The Rs 25,000 crore Maritime Development Fund addresses the historical difficulty of accessing affordable capital, providing long-term, low-interest financing to shipowners and builders. Together, these instruments represent a financial architecture that did not exist a decade ago.

Will This EoI Bridge the Gap?

With these requirements in mind, the Shipping Corporation of India's EoI can be seen as the catalyst designed to bridge these technical and infrastructure gaps through a structured "2+6" build model.

By permitting two vessels to be built at leading international yards while mandating that the remaining six be constructed in India via a technical tie-up, the project forces a direct transfer of proprietary know-how.

This mechanism ensures that Indian engineers and technicians will be embedded in the process—observing, learning, and documenting specialised techniques in cryogenic containment, hull fabrication, and systems integration. The winning international partner must then provide designs, engineering supervision, and performance guarantees for the six vessels built in India.

The international shipbuilder gains access to $950 million in orders and a foothold in India's growing energy import market.

The EoI also addresses the demand uncertainty that has historically deterred shipyard investment. It leverages the 20-year guaranteed cargo contracts from state-owned oil majors like IOCL, BPCL, and HPCL.

This transforms the economics of the project: the ships have assured employment before the first steel is cut.

This vertical integration—bringing together the cargo owner, the fleet operator, and the financier within a single equity structure—de-risks the capital-intensive construction phase.

Indian shipyards can invest in high-nickel metallurgy, specialised welding capabilities, and component supply chains knowing that the vessels will have guaranteed cargo for two decades.

The 20-year contract model is not novel in global shipping; it is how most major LNG and LPG carrier projects are financed. What is novel is India using its position as a major energy importer to create this structure domestically, rather than simply chartering foreign vessels on long-term contracts.

Viewed in totality, India will continue importing LPG in vast quantities regardless. The question is whether those imports will travel on foreign-built, foreign-flagged vessels, or whether the import dependency itself can be leveraged to build domestic capability.

Whether this approach will succeed depends on execution: the quality of the technology partnerships, the absorption capacity of Indian yards, the reliability of component supply chains, and the discipline of the 20-year cargo arrangements.