Economy

India's GDP Series Can't Use UPI Data—Until These Issues Are Addressed

Swarajya Staff

Feb 27, 2026, 02:00 PM | Updated 01:59 PM IST

India processes more real-time digital payments than any other country on earth. Yet, its new GDP series unveiled today, 27 February, will not be making of the UPI (United Payments Interface) data.

In June 2025 for example, UPI processed over 1,840 crore transactions, with merchant payments accounting for more than 1,100 crore transactions and Rs 6.83 lakh crore in value. This is, by any measure, an extraordinary data stream. It is granular, real-time, and covers a significant share of household consumption. One estimate suggests that UPI merchant payments now represent nearly 58 per cent of India's estimated monthly household spending.

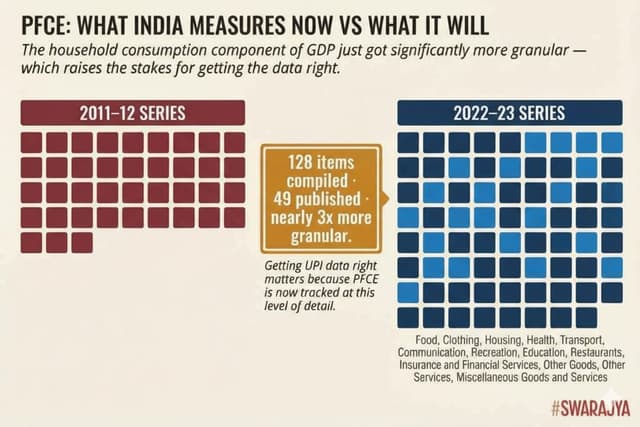

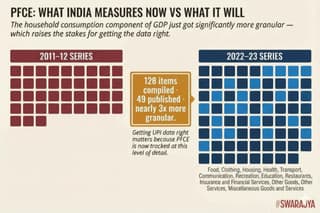

Yet in the new GDP series released today, 27 February, by MoSPI, UPI transaction data will not find a place. The ministry's sub-committee on methodological improvements had looked at UPI as a potential source for estimating Private Final Consumption Expenditure (PFCE) — the household spending component that accounts for more than half of India's GDP — and concluded it was too soon.

The data is there. The problem is that it cannot yet be read appropriately.

The Supermarket Problem

To understand why, consider what UPI actually records.

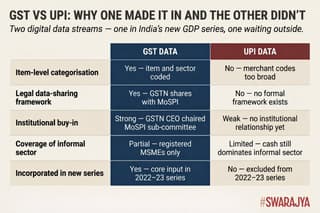

Every transaction is tagged to a Merchant Category Code — a four-digit number assigned to the merchant by their acquiring bank. Code 5411, for instance, refers to "Grocery Stores, Supermarkets." In January 2026, this single code accounted for 25 per cent of all person-to-merchant UPI transactions by volume.

A supermarket sells rice, shampoo, medicines, toys, and stationery. These are goods that belong to entirely different categories of household consumption. For MoSPI to use this data, it would need to know not just that someone paid at a supermarket, but what they bought there. UPI records the payment. It does not record the basket.

This is not a minor inconvenience. It means the most heavily transacted category in the entire UPI system is statistically unusable for the purpose of measuring what Indians consume.

Then there is a more striking anomaly at the other end of the distribution. The merchant code for "debt collection agencies" accounted for just 1.4 per cent of all person-to-merchant transactions in January by volume; but 7.2 per cent by value.

This illustrates the other issue. UPI records financial flows too, not just consumption. Loan repayments, insurance premiums, financial transfers — these move through the same pipes as grocery purchases. Using UPI data for PFCE without being able to separate consumption from financial transactions would introduce significant noise into the very indicator it is meant to improve.

MoSPI's sub-committee put it plainly: once UPI transaction data gets stabilised and the categorisation issues are resolved, it "may be explored for possible inclusion."

What Would "Yes" Look Like?

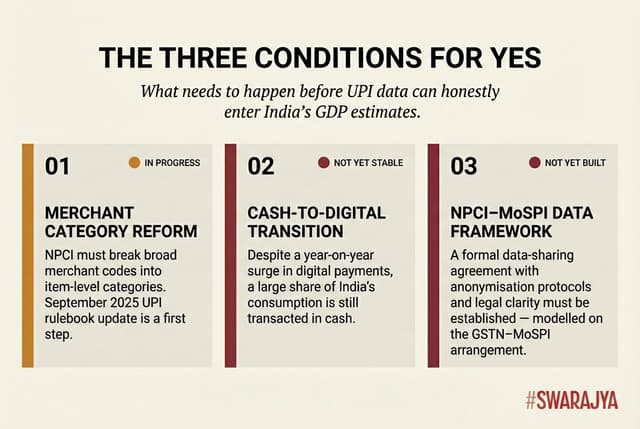

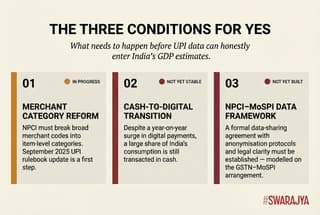

The path from "not yet" to "yes" runs through three distinct problems.

The first is merchant category granularity.

The current system of Merchant Category Codes was not designed to be used as a category for data collection for national accounts. It was designed for payment processing and merchant risk classification. A function which it is performing smoothly.

Merchant category codes are allocated to merchants by acquiring banks and published by NPCI on an "as is" basis, which means there is no uniform national standard for how merchants are classified.

Tweaking this system for data accurate data collection would require a coordinated reform of the MCC taxonomy — not just at NPCI, but across all acquiring banks — to break broad categories like supermarkets into something closer to item-level classification. This is a significant institutional undertaking, but not an impossible one.

NPCI's September 2025 update to the UPI rulebook already introduced a more structured merchant directory taxonomy for high-value transaction categories, suggesting that greater categorisation precision is technically achievable.

The second problem is representativeness. Despite a year-on-year surge in digital payments, a large share of India's consumption — particularly in the informal economy — is still transacted in cash. Using UPI data before the cash-to-digital transition stabilises would produce estimates skewed towards digitally-active consumers. MoSPI has explicitly flagged this, noting that "many people [are] yet to move to UPI from cash."

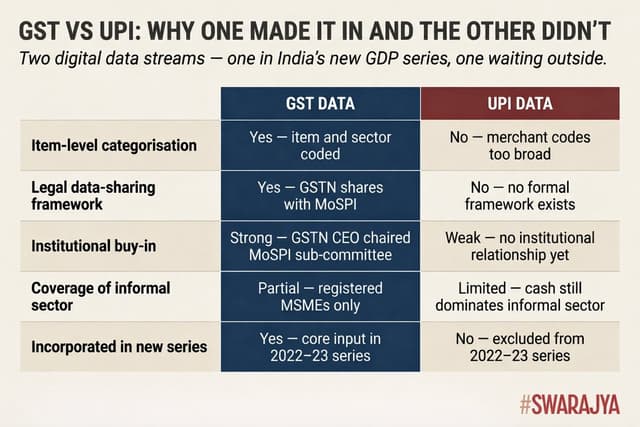

The third problem is institutional. There is no established data-sharing framework between NPCI and MoSPI. GST data entered the new series partly because the GSTN CEO himself chaired the MoSPI sub-committee on new data sources — institutional buy-in built into the process from the start. No equivalent relationship exists between NPCI and the national accounts machinery.

Building one — with appropriate anonymisation protocols, data governance frameworks, and legal clarity — is a prerequisite for any future integration.

UPI Is Already Entering the System — Just Not from the Top

While UPI data hasn't made it into GDP directly, it is entering the statistical system from a different direction.

The Annual Survey of Unincorporated Sector Enterprises (ASUSE) 2026 will, for the first time, track whether informal enterprises accept UPI payments, receive online orders, use e-commerce platforms, or maintain websites and social-media pages.

This is not about using UPI to measure consumption but about using UPI adoption as an indicator of digital formalisation within the informal economy.

As of the day, this is a narrower but more workable use of the data. Rather than trying to read what people buy through their payments, MoSPI is asking: how many of the businesses where they buy things have gone digital?

The answer will generate a baseline that did not previously exist.

Why This Matters Beyond Statistics

It is easy to say that the exclusion of UPI data from the new GDP series shows that India's statistical machinery cannot keep pace with its digital infrastructure. That framing misses the point.

The MoSPI sub-committee's decision was correct. Using poorly-categorised, not-yet-representative payment data to estimate the largest single component of GDP (from the expenditure method) would have introduced new errors in the name of innovation.

The 2015 GDP revision — the last time MoSPI updated the series — was criticised precisely for moving too fast, incorporating new data sources before their reliability was fully established. The caution this time is appropriate.

But caution is not the same as complacency. The conditions under which UPI data becomes usable are not mysterious or abstract or ambiguous. They are specific, achievable, and some of the groundwork is already being laid.

- Merchant category reform is technically feasible.

- Cash-to-digital penetration is deepening every year.

- The ASUSE survey will, from 2026 onwards, generate a digital baseline for the informal sector.

- And the institutional relationship between NPCI and MoSPI that does not yet exist could be built.

The question is not whether UPI data will eventually feed into India's GDP estimates. The question is how long it takes to build the infrastructure that makes it ready to use.