Economy

India's Macro Miracle: Understanding The Country's Broad Growth With Low Inflation

Prof. Vidhu Shekhar

Dec 06, 2025, 10:49 AM | Updated 12:10 PM IST

India is delivering something economists do not expect from a large economy. High growth. Very low inflation. At scale.

This combination is so unusual that standard macro models struggle to classify it. At a moment when major economies are navigating weak expansion, persistent price pressures, or structural drag, India has assembled a configuration that is almost never observed outside small, nimble economies or short-lived booms. It is expanding rapidly while keeping inflation remarkably subdued.

For a country that once lived with recurring inflation spikes and periodic macro scares, this represents a structural break. And it is not a statistical quirk or a fortunate global cycle. It is the result of a decade-long strengthening of institutions, infrastructure, balance sheets, and digital architecture. India's macroeconomic moment is becoming a genuine macro transformation.

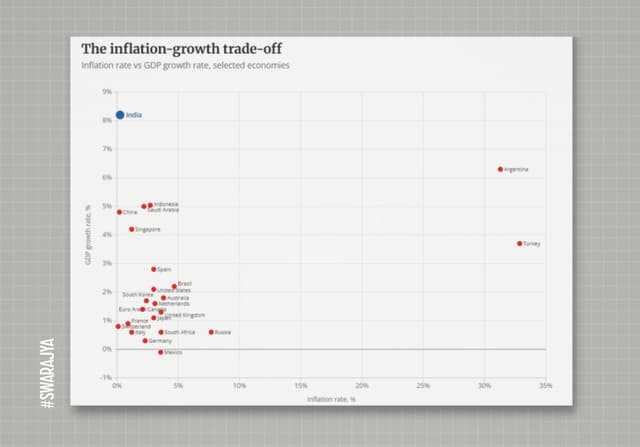

A Growth Performance Without Contemporary Parallel

The numbers are unambiguous. India grew at 8.2% in July-September FY2025-26, extending a multi-year stretch of 6-8% expansion. No other major economy matches this combination of speed and continuity. The United States is slowing. China's model is under strain. Europe is stagnant. Most G20 economies are growing at a fraction of India's pace.

At this scale, maintaining high growth itself is notoriously difficult. Yet India is doing so with an additional surprise: inflation has not risen.

This defies the historical pattern. China's boom in the 2000s generated rising price pressures; Korea's 1980s expansion did the same; Japan's high-growth decades were never free of overheating; even America's 1984 rebound carried pronounced inflation risks.

India is breaking from that script. Headline inflation has mostly held within a 4-5% band for last several years, despite inflationary pressures from covid supply chain hit. In several months of 2025, it dipped below 3%. October's 0.25% print is the lowest in modern times. Wholesale inflation has hovered near zero, signalling minimal cost pressure across supply chains.

A large economy achieving this combination is close to unprecedented. This undoubtedly reflects a new equilibrium.

The Core Explanation: A Step-Change in Supply Capacity

The central fact behind this configuration is simple: India's supply capacity has expanded faster than demand. Few emerging economies manage this. Most are constrained by transport bottlenecks, volatile food supply, fragile energy systems, and regulatory frictions that turn demand upswings into inflation.

India has spent a decade reducing precisely these constraints.

1. Infrastructure That Reduces the Cost of Scale: The build-out of highways, expressways, airports, ports, freight corridors, and digital fibre has changed the production backbone. Goods move faster. Inventory cycles shorten. Regional markets are better connected. Manufacturing and services both benefit from lower friction and higher productivity.

This shifts potential output upward. And when potential output rises faster than actual output, inflation stays contained.

2. A Targeted Industrial Push Through PLI: The Production-Linked Incentive schemes have reinforced this supply transformation. By incentivising scale production in electronics, pharmaceuticals, autos, renewables, and capital goods, PLI has catalysed fresh investment and expanded domestic manufacturing capacity.

The macro consequence is direct: more output, deeper supply chains, and a broader production base that accommodates strong demand without fuelling inflation. PLI has become a structural enhancer of potential growth.

3. A Unified National Market Through GST: GST has integrated India into a single market, eliminating cascading taxes and reducing interstate frictions that once locked up inventories for days. Check-post delays have virtually disappeared. Logistics costs have fallen, supply chains have become more efficient, and firms now operate with far lower working-capital stress.

This integration has further boosted productivity and strengthened the deflationary forces already created by India's digital architecture.

4. Digital Public Infrastructure as a Deflationary Force: Aadhaar, UPI, the GST invoice system, FASTag, and the Account Aggregator framework have rewired transaction flows. They cut delays, reduce intermediary margins, improve compliance, and increase transparency. These mechanisms constitute a structural productivity shock that keeps price pressures moderated even during high-demand periods.

This digital architecture has become a structural source of productivity gains, effectively acting as a deflator in the broader economy.

5. Balance-Sheet Repair Across Banks and Firms: This is another major shift. Gross NPAs have fallen from 11.5% in 2018 to 2.6%, the lowest in over a decade. Corporate deleveraging and the Insolvency and Bankruptcy Code have cleaned up legacy stress. Banks are healthier and better capitalised.

A clean financial system allows firms to expand output without raising prices to defend margins. And when credit growth is supported by sound balance sheets, it fuels investment rather than instability.

6. Demography as a Stabiliser: India's labour force continues to grow. Unlike China, Korea, or Japan during their rapid-growth phases, India is not constrained by labour shortages. A steady flow of workers helps the economy expand without triggering wage-driven inflation.

This combination of capacity, liquidity, and labour supply forms the basis of the present macro moment.

Strong Demand Without Overheating

India's domestic demand profile reinforces price stability. Private consumption has recovered steadily but not exuberantly. Household leverage remains contained. Corporate and MSME credit growth is healthy but not speculative. Real estate is expanding without a leverage-driven boom.

The anchor is public capital expenditure. Government investment has boosted demand while simultaneously raising productive capacity. This is fundamentally different from consumption-led booms that create inflation. Public capex has crowded in private investment, generating a reinforcing cycle of infrastructure expansion and corporate growth.

Demand is strong. But it is also disciplined.

Inflation Is Structurally Anchored

Inflation in India today is shaped far more by structural forces than by monetary policy. Supply shocks now tend to dissipate instead of cascading and anchored expectations are visible across sectors. Inflation has become less sensitive to relative price shocks because supply elasticity has improved across food, manufacturing, and services.

India is increasingly becoming an economy in which inflation is governed by productivity gains, efficient delivery systems, and improved supply elasticity rather than by stop-start cycles of monetary tightening.

Fiscal policy has reinforced this environment. India maintained notable discipline even during COVID, avoiding the broad, cash-heavy stimulus that fuelled post-pandemic inflation elsewhere. Welfare expanded, but within a responsible fiscal envelope.

And, crucially, a substantial share of support was provided in kind through foodgrain distribution and essential services. This protected household consumption while preventing an inflationary surge in discretionary demand.

The Direct Benefit Transfer architecture strengthened this effect. By eliminating leakages, removing ghost beneficiaries, and tightening subsidy flows, DBT ensured that welfare spending translated into real support rather than excess liquidity circulating through informal channels. Less leakage means less artificial demand and, therefore, less price pressure.

Inflation outcomes today reflect this combination: structural efficiency, fiscal discipline, targeted welfare, and cleaner delivery mechanisms. Monetary policy is not the primary story. The structural drivers are.

Global Tailwinds Have Helped, But They Are Not the Driver

Commodity prices have softened. Edible oils, metals, chemicals, and even crude have eased. This certainly supports disinflation.

But a decade ago, similar price relief would not have translated into domestic stability because bottlenecks absorbed the gains. Today, the supply engine is strong enough to amplify global relief.

Global winds have been favourable. But they are not the cause of India's macro equilibrium. They are an accelerant.

A Stronger and More Resilient External Sector

India's external metrics are now among its greatest macro strengths. FX reserves near $690 billion offer substantial insulation. Services exports reached $387 billion in FY2024–25, with a surplus of $189 billion, offsetting more than two-thirds of the merchandise deficit.

The rupee has faced pressure in 2025, but the broader buffers (large reserves, a sizable services surplus, and relatively low external debt) have prevented currency movements from spilling into inflation or financial instability.

This is a complete reversal from 2013. India is no longer exposed to sudden-stop dynamics, short-term external leverage, or currency-driven price shocks. External stability is now embedded in the macro regime.

A Distinct Model Among Large Economies

Comparisons with earlier high-growth episodes are inevitable, but India's model is structurally different. China relied on credit-intensive manufacturing. Korea depended on export-led industrialisation. Japan operated under unique post-war conditions.

India is combining services strength, digital infrastructure, diversified domestic demand, prudent macro policy, and a large labour pool, all within a democratic framework. No major economy delivers this mix with such low inflation volatility.

Existing analytical templates do not fully capture this trajectory.

A Strategic Window. And a Responsibility

India now has macro headroom. It can grow at 8%+, with the possibility of double-digit growth in between, for several years without triggering instability. This creates a strategic window.

If the country sustains reforms in logistics, energy, factor markets, capital markets, and state capability, it could plausibly reach $7 trillion by 2030.

India's growth is already altering the global economic order. The size jump could further amplify it.

Such windows are rare. China had one in the early 2000s. And it reshaped global manufacturing. India's moment has similar potential, strengthened by digital scale, financial stability, and institutional depth.

This is not a fortunate disinflation or a cyclical upswing. It is the consequence of sustained reform. The task now is to use this moment to build a future aligned with India's scale and ambition.

India's macro miracle is real. And the opportunity ahead is historic.

Dr. Vidhu Shekhar holds a Ph.D. in Economics from IIM Calcutta, an MBA from IIM Calcutta, and a B.Tech from IIT Kharagpur. He is currently an Associate Professor in Finance & Economics at Bhavan's SPJIMR, Mumbai. Previously, he has worked as an investment banker and hedge fund analyst. Views expressed are personal.