Economy

The $170 Billion Gap: Can India Drill Its Way To Energy Independence?

Raghavan S Rao and Venu Gopal Narayanan

Feb 11, 2026, 07:00 AM | Updated Mar 04, 2026, 03:56 PM IST

Ten days after speaking at the Prime Minister's Roundtable with Global Energy Leaders on the sidelines of India Energy Week in Goa, Anil Agarwal posted a message on X that was designed to provoke. "The world doesn't want India to produce," the Vedanta Group chairman wrote on 9 February 2026. "It only wants India to be a market."

Within hours, the line had ricocheted across Business Today, India TV, Zee News, and social media. The post laid out a geopolitical argument ("India is vulnerable because we import 90% of our oil and gas. We are surrounded by sea on three sides which can be blockaded in hostile times") and a call to arms ("We must push back. We must fight to be self-sufficient"). But Agarwal was not merely performing for his followers. He was articulating a thesis he has refined over fifteen years in the upstream oil business, one gaining adherents across India's strategic establishment: that the country's extreme dependence on imported hydrocarbons is not an immutable geological fact but a policy choice, and a disastrous one.

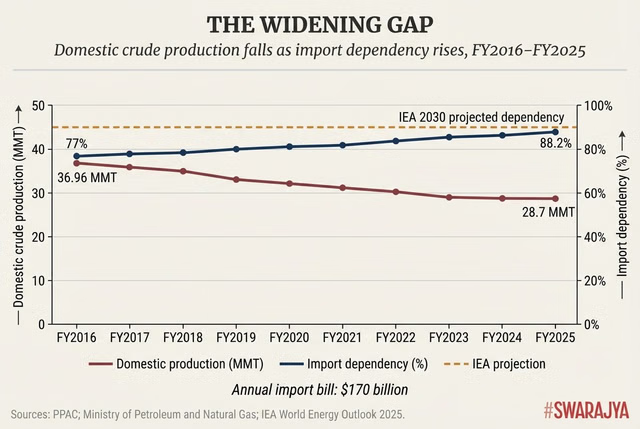

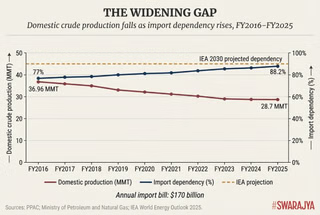

The numbers that underpin his argument are stark. India imported 88.2 per cent of its crude oil in FY2025, up from 77 per cent a decade ago. The annual import bill exceeds $170 billion, roughly equivalent to the combined budgets for defence, education, and health.

Meanwhile, domestic crude production has fallen steadily, from 36.96 million tonnes in FY2016 to 28.7 million tonnes in FY2025, even as the country has added refining capacity at a furious pace, becoming the world's fourth-largest refiner. India processes the world's oil. It just cannot find its own.

Agarwal's company, Cairn Oil and Gas (the upstream arm of Vedanta), is the most prominent player in the private sector. The PM's Roundtable at India Energy Week was Agarwal's first public appearance after the death of his son Agnivesh.

Vedanta holds 62 exploration blocks covering more than 61,000 square kilometres and has announced plans to invest up to $5 billion to boost Rajasthan output fivefold, from approximately 100,000 barrels of oil equivalent per day to 500,000. At CERAWeek 2025 in Houston, in conversation with Daniel Yergin, Agarwal declared that India needed "thousands of drilling rigs operating across the country."

It is a seductive vision. But between the vision and the geology lies a chasm of uncertainty that neither Agarwal's rhetoric nor government press releases adequately acknowledge.

To understand what India might be sitting on, start with the map. The country has 26 recognised sedimentary basins stretching across 3.36 million square kilometres of land and ocean. The DGH classifies seven as commercially producing (including Mumbai Offshore, Krishna-Godavari, Cambay, Assam-Arakan, and Rajasthan), five with known hydrocarbon shows but no production, and thirteen or more as relatively unexplored.

ONGC has mapped all of them; this is not uncharted territory. But the gap between reconnaissance-level seismic surveys and the intensive drilling required to prove commercial reserves is vast. Roughly 10 per cent of India's total sedimentary area is under active exploration.

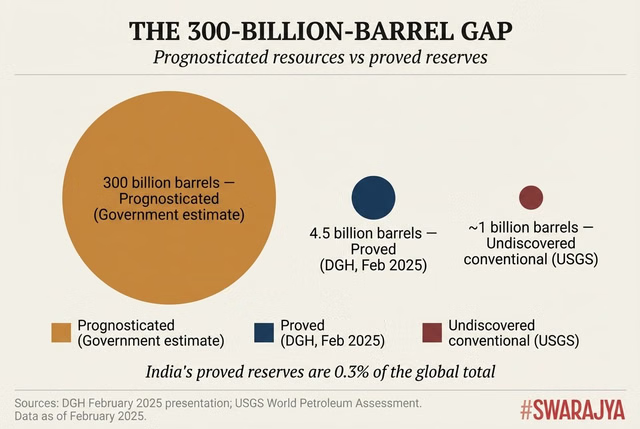

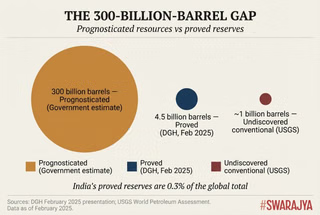

Government estimates place India's "prognosticated" hydrocarbon resources at 41.87 billion tonnes of oil equivalent, roughly 300 billion barrels. This is the figure Agarwal and others cite when arguing that India has more than 30 times Guyana's proven reserves. Petroleum minister Puri has described India's exploration opportunity as worth $100 billion in investment alone. S&P Global Commodity Insights has reported that just four largely unexplored basins, Mahanadi, Andaman Sea, Bengal, and Kerala-Konkan, could hold up to 22 billion barrels of recoverable oil equivalent, which would exceed the Permian Basin's remaining reserves.

These are large, exciting numbers. They are also, in the candid assessment of several geologists and petroleum economists interviewed for this article, deeply misleading when presented without qualification.

India's actual proved crude oil reserves, the barrels that have been drilled, appraised, and deemed commercially recoverable, stand at approximately 4.5 billion, according to the DGH's own February 2025 data. That is 0.3 per cent of the global total. The gulf between 4.5 billion proved barrels and 300 billion prognosticated barrels is the gulf between what India knows it has and what it hopes the subsurface might contain. How to turn the theoretical into the tangible is the $170 billion question.

Prognosticated resources are theoretical estimates: extrapolations from analogues elsewhere, seismic surveys of varying quality, and educated guesswork. Before a single barrel enters the "proved reserves" column, it must pass through successive filters of exploration, appraisal, and commercial viability, each of which eliminates the vast majority of initial estimates.

The most authoritative external assessment comes from the United States Geological Survey, whose evaluation of ten Indian basins yielded a mean estimate of approximately one billion barrels of undiscovered conventional oil, roughly 300 times smaller than the government's headline number. The two figures measure different things, but the gap is a caution against treating 300 billion barrels as a proven endowment waiting to be drilled.

"The 300-billion-barrel number gets repeated so often it has acquired the status of fact," said one senior petroleum geologist who has worked on Indian basin evaluations and requested anonymity. "In reality, we will not know what is there until we drill. That is the nature of exploration. The honest answer is that India's potential is genuinely unknown, which is both the problem and the opportunity."

The scepticism runs deeper among those who have tried to make the economics work on the ground. One senior oil industry executive who spent decades in India's upstream sector offered a blunt assessment: "The geology of our frontier basins does not suggest the presence of commercial shale plays in American volumes."

He described working on an unconventional gas prospect in the Rewa basin of Madhya Pradesh, which the government offered to a foreign operator on generous terms. "I stood on my head trying to make the economics work. I involved a reputed Canadian consulting firm to cross-check my calculations. They came to the same conclusions. We had to turn the project down." The potential that does exist, he argued, is more likely offshore, particularly in the Andaman and Nicobar deep waters, but even there, the greater probability is of encountering gas rather than oil.

If the potential is uncertain, the track record of what systematic exploration can achieve in India is not. That evidence comes overwhelmingly from a single source: the Barmer Basin in Rajasthan.

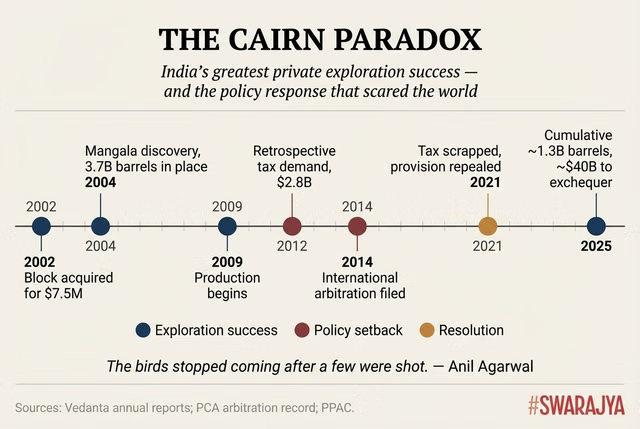

In 2002, Cairn Energy, a Scottish independent not yet part of Vedanta, acquired Block RJ-ON-90/1 for $7.5 million. Shell had walked away from the block. What Cairn's geologists saw in the seismic data persuaded them to drill, and in 2004 they struck Mangala, the largest onshore oil discovery in India in more than two decades, with an estimated 3.7 billion barrels of oil in place.

Production began in August 2009, and within a few years the Rajasthan block was contributing more than a quarter of India's total domestic crude output. Cumulative production has reached roughly 1.3 billion barrels; Cairn has contributed approximately $40 billion to state and central exchequers.

But the Cairn story also illustrates the countervailing forces. The retrospective tax demand of 2012, a $2.8 billion claim on Cairn Energy for a 2006 corporate restructuring, became one of the most damaging episodes in Indian investment history. Cairn won at international arbitration; India eventually scrapped the provision in 2021. But the damage was not merely financial.

Agarwal has used the metaphor of Keoladeo National Park, where migratory birds stopped coming after a few were shot. "Even one court case or notice in the public domain catches like fire in the world," he has said. The retrospective tax episode was heard clearly in Houston, Calgary, and London. International oil companies have stayed away.

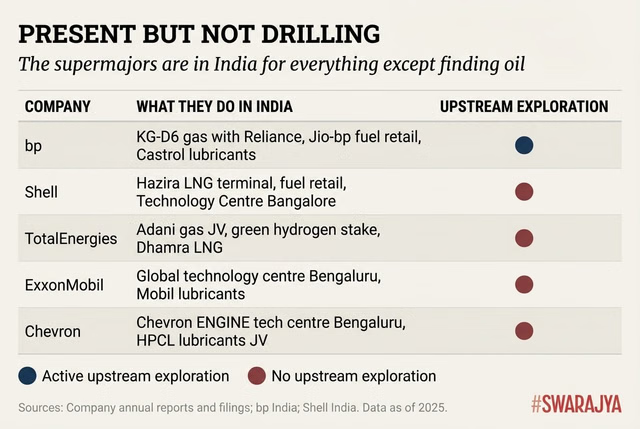

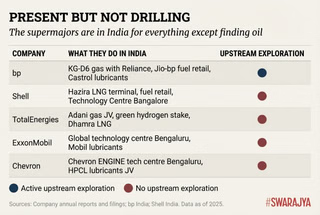

This is the puzzle at the heart of India's exploration deficit. ExxonMobil, Chevron, Shell, TotalEnergies, bp, Equinor: the companies that transformed Guyana, the Gulf of Mexico, and the Permian Basin are conspicuous by their absence from upstream exploration.

They are not avoiding India: Shell operates the Hazira LNG terminal and a global technology centre in Bangalore; TotalEnergies holds stakes in Adani's gas distribution and green hydrogen ventures; ExxonMobil and Chevron both run major technology centres in Bengaluru; bp partners with Reliance on fuel retail and KG-D6 gas production. The supermajors are happy to sell India oil, market its gas, and blend its lubricants. They are simply unwilling to hunt for hydrocarbons in Indian acreage.

The Open Acreage Licensing Policy, introduced in 2017, has completed nine bid rounds, awarding 172 blocks. But the overwhelming majority of winners have been ONGC and Oil India, the same state-owned firms whose declining production prompted the reforms.

Why won't the majors explore? Fiscal terms, while improved, are still less competitive than Brazil, Guyana, or West Africa. The KG-D6 arbitration, with government claims against Reliance and bp approaching $30 billion, sends a message about contract sanctity. And India's frontier basins are genuine wildcats, lacking the accumulated well data that reduces uncertainty in mature provinces.

The comparison with Guyana is instructive precisely because it reveals both the opportunity and the difficulty.

In May 2015, ExxonMobil's deepwater drillship struck oil in the Stabroek Block offshore Guyana, a country of 800,000 people with no hydrocarbon history. More than 30 additional finds followed. By late 2025, Guyana was producing 900,000 barrels per day, with a trajectory toward 1.7 million bpd by 2030.

The Stabroek Block's 11 billion barrels of estimated recoverable resources have given a tiny South American nation the highest GDP growth rate on earth, an average of 47 per cent annually from 2022 to 2024.

Agarwal and others point to Guyana as proof of what frontier exploration can yield. India's sedimentary basin area is roughly 125 times larger than the Stabroek Block, and initial drilling in the ultra-deepwater Andaman Sea has established a petroleum system potentially analogous to producing basins in Myanmar and North Sumatra.

But the Guyana comparison also exposes what India lacks. ExxonMobil explored the Stabroek Block under a production-sharing agreement of extraordinary generosity: a 2 per cent royalty, a 50-50 profit split after cost recovery, and tax exemptions that make the effective government take among the lowest in the world. Those terms attracted the very company with the capability to find the resource. India's fiscal apparatus reflects a justified desire to capture fair value. But the trade-off is real: more demanding terms attract fewer world-class explorers.

There is a subtler lesson too. Guyana's success was the product of decades of prior geological work; Exxon's predecessors had explored the basin since the 1960s. India's frontier basins have had a fraction of that investment in basic data. The government's Mission Anveshan programme, launched in October 2024 with a ₹792 crore budget to survey seven basins, is a start, but modest relative to the unknowns.

The model Agarwal invokes most passionately, however, is not Guyana but the American shale revolution, and here the analogy is both more compelling and more problematic.

Two decades ago, the United States imported 60 per cent of its oil and was widely assumed to be in permanent decline. The transformation was achieved not by state-owned enterprises but by entrepreneurs, many of them small, stubborn, and willing to fail.

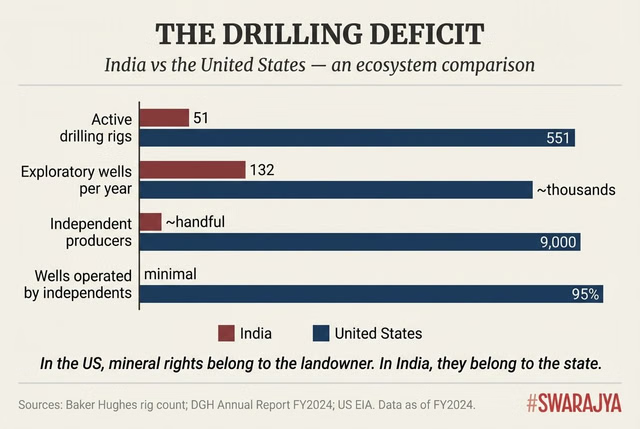

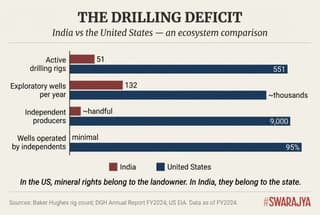

George P. Mitchell spent 17 years cracking the code for extracting gas from the Barnett Shale; the technology was rapidly adopted across the Bakken, Eagle Ford, and Permian basins. Today, roughly 9,000 independent producers operate 95 per cent of US wells and produce 85 per cent of its oil, more than 13.4 million barrels per day, more than any country in history.

Agarwal's vision of "thousands of drilling rigs" deliberately echoes this model. And there is a structural truth here: the US revolution happened because the regulatory environment rewarded risk-taking. Mineral rights belong to the landowner, not the state. Federal tax credits, fast permitting, deep capital markets, and a century of accumulated well data reduced barriers to entry.

India has virtually none of these enabling conditions. All subsurface mineral rights belong to the state, which means a farmer whose land sits above a promising formation has no financial stake in drilling; it is pure nuisance, threatening water tables and crops with no offsetting royalty.

In Texas, a landowner can grow wealthy from a productive well; in Tamil Nadu's Cauvery Delta, farmers have fought ONGC operations so fiercely that the state government declared the region a Protected Special Agricultural Zone, banning new exploration entirely.

Capital markets for upstream oil and gas are thin. Environmental clearances routinely take years. The number of active drilling rigs stands at roughly 51, compared to 551 in the US. India drilled 132 exploratory wells in FY2024; the US drills thousands annually.

The senior industry executive who worked on the Rewa basin prospect put the challenge in starkly practical terms: "Which Indian onshore sedimentary basin will accommodate these 'thousands of rigs'?" It is a question that proponents of the shale analogy have yet to answer.

More fundamentally, the shale revolution rested on an ecosystem: pipelines, oilfield services, trained geologists, an established regulatory framework, built over 165 years and four million wells. India cannot replicate this overnight.

What it can do, Agarwal argues, is begin: by expanding active exploration licences to 2,000, cutting the effective tax burden to 30 per cent, extending licence terms to 70 years, and shifting the regulatory posture from oversight to facilitation.

The cost of inaction is measurable and accelerating. The IEA projects domestic production will decline to 540,000 barrels per day by 2030 without major new discoveries, even as demand rises toward six million bpd.

Strategic petroleum reserves cover nine to ten days of imports, far below the IEA's 90-day standard. The geopolitical exposure is already being weaponised: the February 2026 trade framework with the US requires India to curtail Russian oil purchases in exchange for tariff relief, with a monitoring clause empowering Washington to snap duties back if compliance lapses.

Managing the three-way balancing act between Washington, Moscow, and the Middle East has become, in the words of one serving diplomat, "the primary job of the External Affairs Ministry." In the 1960s, President Johnson weaponised India's dependence on American wheat under PL-480 to extract geopolitical compliance. Today the commodity is different; the dynamic is the same.

India's subsurface potential is genuinely unknown, and the only way to resolve the uncertainty is to drill, far more, far faster, and in far more places than it currently does. The government's recent reforms, OALP, Mission Anveshan, the Oilfields Amendment Act's stabilisation clause, are genuine steps forward. But they remain incremental adjustments to a system that has failed to attract the capital India's basins require.

The question is whether India will create conditions so attractive that the world's best explorers consider it irrational not to participate: competitive fiscal terms, contract sanctity across electoral cycles, regulatory processes measured in months not years.

Any honest reckoning must also acknowledge what ONGC has achieved. Over seven decades, its world-class geologists mapped every one of India's 26 sedimentary basins, built the offshore Mumbai High into one of Asia's great producing fields, and conducted major deepwater drilling campaigns at enormous cost, including in waters off the east coast and Andaman Sea, that, while commercially unsuccessful, generated irreplaceable subsurface data. ONGC's experience is not evidence of timidity; it is evidence of how geologically challenging India's frontier basins actually are, and it weighs heavily on future exploration expenditure decisions across the industry.

Agarwal's formulation, that India needs only the right policy environment to unlock its potential, is self-interested but not wrong. What he leaves unsaid is that the geological evidence for 300 billion barrels is thin, that the shale analogy papers over fundamental structural and geological differences between the American Permian basin and Indian frontier basins, and that even the best reforms will take a decade to translate into material production.

India's energy future will be decided, basin by basin and well by well, by whether the country and private enterprise summons the courage to find out what lies beneath its feet. The drill bit does not do politics. But everything that determines where and whether it turns does.

Raghavan S Rao is a public policy consultant and student of economics. Venu Gopal Narayanan (@ideorogue) is an independent upstream petroleum consultant who focuses on energy, geopolitics, current affairs and electoral arithmetic.