Economy

Transformative, But States May Nullify It All: Prof Prasanna Tantri On Budget 2026

Diksha Yadav

Feb 04, 2026, 01:26 PM | Updated Mar 04, 2026, 03:54 PM IST

The Union Budget 2026-27 arrived amid muted reactions from people describing it as "boring" due to the absence of headline-grabbing income tax announcements. But this assessment misses the forest for the trees.

In a detailed conversation with Professor Prasanna Tantri, Associate Professor of Finance at the Indian School of Business, on the What This Means podcast, what emerges is a picture of genuine structural transformation at the central government level, one that may be entirely nullified by state government profligacy.

The Big Picture: Government Is Withdrawing

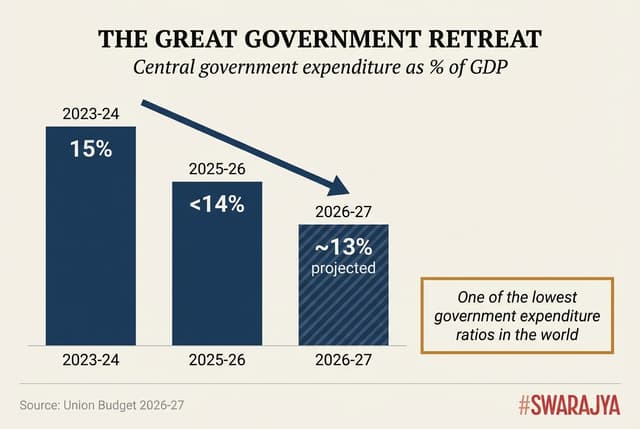

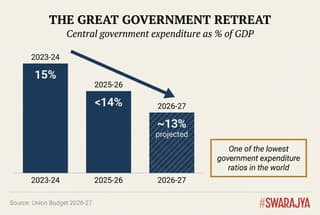

The most significant shift in this budget, according to Prof Tantri, is the central government's deliberate retreat from the economy. In 2023-24, government expenditure had reached 15 per cent of GDP, one of the highest levels, exceeding even UPA-era spending after COVID. The revised estimates for 2025-26 show spending at Rs 49.6 lakh crore on a nominal GDP of Rs 354 lakh crore, bringing the ratio below 14 per cent. For 2026-27, the total expenditure projection is Rs 53.5 lakh crore against a GDP of Rs 394 lakh crore, likely to come in even lower at around Rs 52 lakh crore based on past patterns.

"Government expenditure below 14 per cent of GDP is one of the lowest in the world," Tantri notes. "This allows so much space for the private sector. Government can do lot more by its absence than its presence."

He points to the service sector as evidence: it has thrived precisely because successive governments never bothered to "help" it. "Moment government starts bothering about any sector, you can be reasonably assured that it will be messed up."

Defence: The Second Major Positive

The defence budget has finally crossed 2 per cent of GDP, up from less than 1.8 per cent previously, with a 20 per cent increase in capital expenditure. Tantri and his friend Aditya Kolekar had argued in a Times of India article that defence research has the highest multiplier effect among all government spending categories.

"Between building a road to nowhere versus defence research, this has the much higher multiplier effect on various sectors," he observes, though he hoped for even more, perhaps Rs 8-10 lakh crore eventually. Europe is moving towards 3-4 per cent of GDP; India should follow.

Where the Cuts Hurt: Essential Schemes vs Capex Ideology

The budget documents reveal one striking statistic on state capacity: of 127 major programmes announced last year, the government missed outlay targets for 95 (excluding roads and railways), cutting allocations from ₹10.5 trillion to ₹8.3 trillion. Prof Tantri explains that part of this is mechanical. Inflation came in lower than expected, so both tax collections and expenditure fell. But the pattern of cuts reveals troubling priorities.

The Nal Pe Jal scheme saw allocation of Rs 70,000 crore but spending of only Rs 10,000 crore, a tacit acknowledgement that the scheme is not working. State government capex received Rs 4.3 lakh crore allocation but only Rs 3 lakh crore was spent. These cuts are understandable. What is concerning are the cuts to genuinely essential programmes.

Awaas Yojana, Swachh Bharat, and Ayushman Bharat (flagship schemes from Modi's first term) all saw actual spending fall 20-50 per cent below allocation. "I would have cut capex straight away by a lakh crore than cutting these essential schemes," Prof Tantri argues.

This reflects what he calls "capex ideology," the notion that anything classified as capital expenditure is automatically good while revenue expenditure is bad. "Come on, Ayushman Bharat is not a bad expenditure. This is why we have government. What is spent on judiciary is not bad expenditure. Imagine you have more judges recruited. The multiplier effect is going to be far higher than any kind of road you can make."

Projects like Vande Bharat, if they generate positive returns, should borrow from markets rather than consume taxpayer money. "Government needs to step in when we have this thing called market failure": healthcare, education, rural connectivity where private investment will not go. Building random airports that shut down (14-15 of 84 have already stopped functioning) is not productive capex.

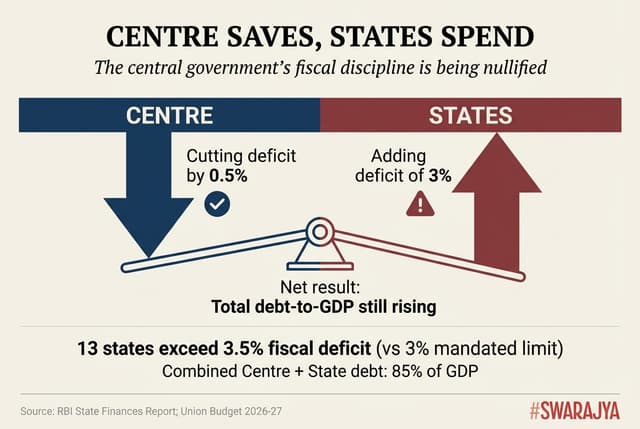

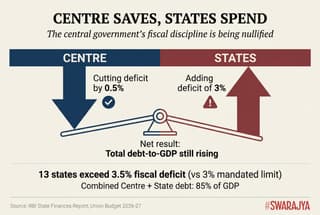

Where the Optimism Ends: The State Government Problem

Here is where the optimism ends. While the central government has achieved fiscal discipline, state governments are borrowing another 13-14 trillion rupees. Thirteen states have fiscal deficits exceeding 3.5 per cent, above the mandated 3 per cent limit. Combined central and state debt stands at 85 per cent of GDP.

"Central government will cut half a per cent. States will add 3 per cent. What's the point? Total debt to GDP is going up only."

The numbers are stark: total savings in the economy run around 90-95 trillion rupees. Government borrowing absorbs 30 trillion. With no significant FDI coming in and another 10 trillion needed for depreciation and maintenance, where does private investment capital come from?

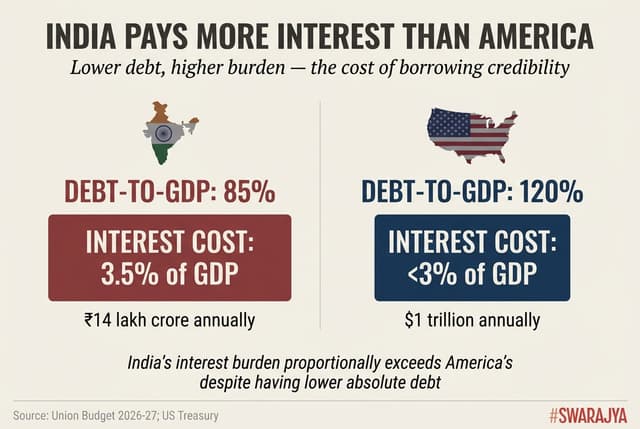

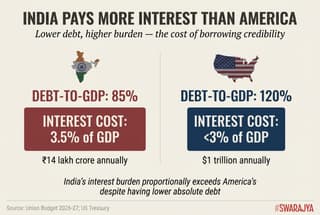

Central government interest expense is already Rs 14 lakh crore, or 3.5 per cent of GDP, on total revenue of Rs 34 lakh crore. For comparison, the United States, with 120 per cent debt-to-GDP, pays only 3 per cent in interest. India's interest burden as a proportion is higher than America's despite having lower absolute debt.

The cycle of freebies, which Prof Tantri traces back to the 2008 debt waiver that consumed 2 per cent of GDP, has spread to every state. PM-KISAN started it at the central level in 2018, Karnataka followed in a big way, then Telangana, Maharashtra, Jharkhand, Bengal. Now every state wants to give cash to women. This is not partisan: BJP-ruled states are doing it too.

"My definition of freebie is if it is not solving a market failure, then it's a freebie," Prof Tantri clarifies. PM SVANidhi, which gave loans of 10,000-50,000 rupees to street vendors who had no credit access, is not a freebie. It solved a genuine market failure. Randomly transferring 2,000-3,000 rupees for no reason is a freebie.

The RBI Dilemma

The real danger is if the Reserve Bank tries to cushion rising interest rates by printing money. RBI has already printed Rs 6.5 lakh crore of reserve money in the last six months; otherwise, market rates would have risen further. The 10-year government bond yield is at 6.77 per cent, up 50 basis points despite RBI rate cuts. The 30-year bond yields 7.4 per cent.

"Printing money is not the answer, RBI should let the interest rates go up. Let these policymakers suffer. Otherwise we will suffer for long term."

When the government's own projections expect 4 per cent inflation next year and the repo rate is 5.25 per cent, real rates are only 1.25 per cent, historically low. There is no scope for cutting further. If state government borrowing continues, RBI should raise rates, not cut them.

F&O Trading: Right Problem, Wrong Solution

Finance Minister Sitharaman called speculative F&O trading sattebazi (gambling), echoing Prof Tantri's earlier position that retail investors dabbling in derivatives they do not understand are worse off than Dream11 players. The problem is real: retired people treating complex derivative payoffs as free money and losing their savings.

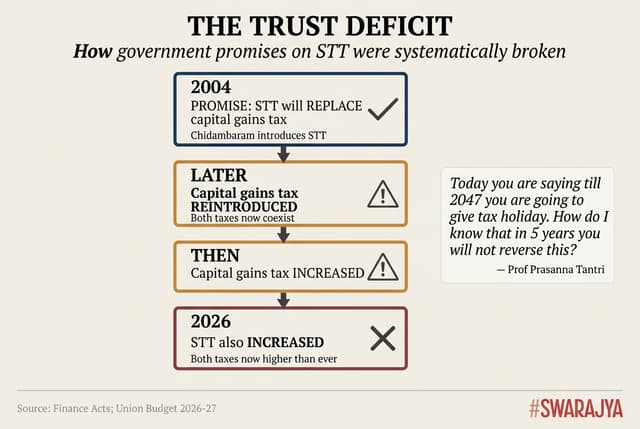

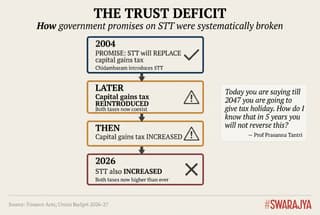

But the solution, increasing STT (Securities Transaction Tax), is wrong. The right approach was for SEBI to increase lot sizes and margin requirements, pricing out unsophisticated retail investors while letting sophisticated traders continue. Instead, the STT hike taxes everyone, including those using derivatives for legitimate hedging.

More troublingly, this represents a breach of trust. When former Finance Minister Chidambaram introduced STT, the explicit promise was that it would replace capital gains tax to encourage long-term investing. The Indian state went back on this by reintroducing capital gains, then increasing both capital gains and STT. "If you do that, people will not trust you. Today you are saying till 2047 you are going to give tax holiday. How do I know that in 5 years you will not reverse this?"

Sovereign Gold Bonds: A Plain Breach of Contract

The change in tax treatment for Sovereign Gold Bonds is, in Prof Tantri's words, "plain breach of contract." In 2015, the government looked at ten years of flat gold prices and offered a compelling deal: instead of buying physical gold, invest in bonds that appreciate with gold prices, earn 2.5 per cent annual interest, and pay no tax on maturity gains.

Gold prices subsequently surged. Last year, the government tried reducing customs duty to bring prices down. It did not work since gold prices are determined globally, not by India. Now, having lost perhaps Rs 1-1.5 lakh crore on the scheme, the government wants to claw back some amount by taxing secondary market purchasers who were never told the tax exemption applied only to original RBI allottees.

"Those who bought from the secondary market, they had no idea that this is going to be taxed. That is bad." The government made a bad call and should pay for it, just as any private person or company would. Instead, because they "hold the gun" of taxation, they are punishing citizens for their own mistake.

The amount involved, perhaps Rs 10,000-20,000 crore, is trivial in a Rs 53 lakh crore budget. But the damage to trust is significant. "Any kind of thing where people see that state is cheating creates a lot of dissatisfaction." This, Prof Tantri suggests, should be rolled back.

US-India Trade: Competition Is Coming, And That's Good

The Truth Social posts about $500 billion in trade should be taken with a pinch of salt. India's total imports are only $700-800 billion. But the direction of travel matters more than the headline numbers. Trump correctly identified an asymmetry: India charged high tariffs while the US did not reciprocate. Given where negotiations started (50 per cent tariffs threatened), the current outcome of 18 per cent tariffs is far better.

But Prof Tantri's optimism is not about exports. It is about imports. India's protectionist policies have coddled infant industries that remain perpetual infants. A 150 per cent tax on automobiles makes no sense decades after the industry began. FTAs will force competition.

"People are looking at exports. I am looking at imports. Because these guys come in, we have only two choices, either compete or perish."

He recalls the pre-liberalisation era when scooters had to be tilted to start, not because that was the technology, but because protection removed any incentive to improve. There was even an R.K. Laxman cartoon where ISRO engineers suggested tilting a satellite that would not launch. Competition in safety, features, comfort: all will force Indian manufacturers to scale up.

The Verdict

Asked to describe the budget in one word or sentence, Tantri struggles, because the assessment depends on which level of government you are looking at.

"From the central government expenditure point of view, it's transformative. But bring state, everything is nullified."

Eighteen to twenty states are ruled by the same party that controls the centre. The state problem is not about opposition governments being reckless. It is universal. And until that changes, Finance Minister Sitharaman's disciplined fiscal management will be swimming against a tide of state-level profligacy.

The FM delivered on her five-year-old promise to reduce fiscal deficit to 4.5 per cent, something even developed countries rarely achieve. She could have made ten fancy announcements and implemented none; commentators would have been happier. Instead, she chose substance over showmanship. Whether that substance survives the states remains the central question of Indian economic policy.

(This article is based on a conversation between Diksha Yadav and Professor Prasanna Tantri for "What This Means". The full episode is out on Swarajya's Spotify and Apple Podcasts.)

Diksha Yadav is a senior sub editor at Swarajya.