Technology

India's Space Sector Is Booming. Its Supply Chain Is Almost Entirely Foreign.

Karan Kamble

Mar 08, 2026, 06:59 AM | Updated 11:08 AM IST

In 1970, in Middletown, Connecticut, three men set up a small optics workshop.

They had a bedroom air-conditioner that they hauled to the floor each morning to keep the workspace cool enough for precision work.

They had backing from Canon Inc and Wesleyan University to make small optical components. The company was called Zygo Corporation.

Today, Zygo has over 500 employees, a 160,000-square-foot campus, 10 offices on three continents, and its computer-controlled optical metrology technology was used to test and measure the 18 hexagonal mirror segments of the James Webb Space Telescope's primary mirror, the 6.5-metre instrument that captured the deepest infrared images of the early universe.

The humble company became one of the world's premier precision optics manufacturers because the National Aeronautics and Space Administration (NASA) and the Department of Energy gave it early orders, steadily and over decades. First it was for small optics, then for the National Ignition Facility's 1,000-plus metre-class laser optics, and eventually for space payloads.

A point to note: It was not the venture capitalists who were making this bet early. The United States (US) government decided the capability should exist and structured its procurement to create it.

Zygo is not an exception. Ball Aerospace, acquired by BAE Systems in 2024 for $5.6 billion, began in 1956 as a research offshoot of the Ball Corporation, a company best known for making glass mason jars. Early NASA contracts turned it into one of America's premier space instrument manufacturers; it built the primary mirror system for the same James Webb Telescope.

SpectraTime, the Swiss atomic clock firm whose clocks are now failing on India's NavIC satellites, was founded in 1995 as a small outfit in Neuchâtel; European Space Agency (ESA) contracts for the Galileo constellation scaled it into the world's dominant supplier of space-grade atomic clocks.

The MIT Instrumentation Laboratory, now the Draper Laboratory, started as a tiny research unit in 1932; US Navy and NASA contracts made it the birthplace of inertial navigation, from submarine guidance to the Apollo lunar landing system.

There's a pattern here: governments identified the subsystem capability they needed, placed sustained orders, and let the company grow into it.

Where Is India's Zygo?

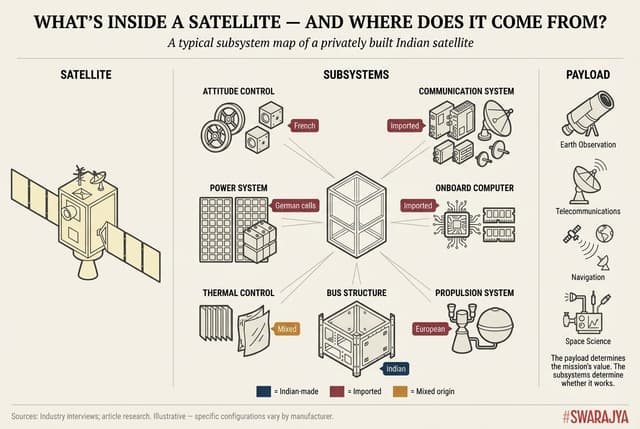

Consider what you may find inside a typical Indian-built satellite today.

The attitude determination and control system (ADCS), the module that keeps the satellite pointed at the right patch of Earth, comes from a French company. The optics are European. The thrusters are from European companies such as Exotrail. The solar cells inside the panels are German. The onboard computer is imported.

And the GPS receiver, the unit that tells a Rs 200-crore satellite where it is in orbit, has, in at least one documented case involving a private satellite builder, been a $13 component sourced from a Chinese manufacturer, probably not radiation-hardened or space-qualified in any rigorous sense.

That last bit, though, is not universal: ISRO and DRDO satellites use Indian-built receivers. But even in those cases, the crucial RF front-ends are Taiwanese, and space-grade COCOM-limit-removed chips cost upwards of $2,000 each. The dependency runs deeper than the unit price suggests.

What is Indian? The bus structure, sometimes. And yes, the integration and the brand.

At present, there is a gap between the brand and the capability.

It is worth examining why India's booming private space sector, about five to six years into the most ambitious liberalisation in its history, is producing a whole lot more satellite and rocket companies than those that make the things that go inside them, almost as if the latter matter less.

The "Space" We Are In

India's private space sector is booming by every conventional measure.

Since the liberalisation of 2020, the number of private space companies has grown from over 50 to over 400.

Total venture funding has crossed $726 million. Skyroot Aerospace, which has raised nearly $100 million, launched India's first privately built rocket. Pixxel, at $96 million, is deploying a hyperspectral imaging constellation. Agnikul Cosmos, at $73 million, is developing a 3D-printed semi-cryogenic engine.

The government has announced a Rs 1,000-crore venture capital fund for the sector. The Cabinet Committee on Security has approved a Rs 27,000-crore military satellite surveillance programme, SBS-3, with 31 of 52 satellites to be built by private firms.

Space startups are on magazine covers. Ministers are photographed at launch pads. India's "SpaceX moment" is a staple of conference rhetoric.

But where is the money really going? The data platform Tracxn tracks over 200 active Indian space tech companies and categorises the top-funded business models as small satellite launch vehicles, satellite imaging services, and satellite communication services.

It is a little concerning to not find components on the list.

In fact, no subsystem-only company appears in any of those top-funded lists. The three highest-funded startups are all building either rockets or complete satellite systems.

The venture capital (VC) architecture of Indian space rewards what space policy expert Chaitanya Giri calls "the glamour": the company that can pitch an end-to-end story, from launch to orbit to data delivery, perhaps with a path to an IPO.

What it does not appear to reward is the company making the gyroscope inside the satellite. Or the atomic clock. Or the onboard computer. Or the precision optics that determine image quality. Or the ADCS that keeps the satellite pointed at a region of interest on Earth.

Giri describes the problem with a cricket analogy. Everyone is chasing the same ball, he says. Dozens of companies are building small satellites, competing with each other rather than cooperating on subsystems. Though, it must be said, this is beginning to change: a recent IN-SPACe-led public-private partnership has brought Pixxel, Dhruva Space, SatSure, and Piersight together as a consortium to build India's national Earth observation constellation.

"Systems integrators are bound to fail," argues an accomplished engineer in the Indian space technology sector who did not want to be named, "because what happens is the French company gives attitude control, solar panels come from the US, thrusters from a European startup — you put all of this together, and you don't understand how any of it works."

The satellite company in India then becomes an assembler, not a manufacturer. The intellectual property (IP), the knowledge that makes a space programme strategically valuable and the country aatmanirbhar (self-reliant), stays abroad.

This is concerning because the distinction between integration and manufacturing is the distinction between weak IP and strong IP.

A satellite bus, the structural platform onto which you bolt components, is commodity engineering. Any reasonably competent team can learn to build one. But a space-grade gyroscope, a rubidium atomic frequency standard, an adaptive optics system, a radiation-hardened onboard processor: these are hard-won capabilities that take decades to develop and that confer lasting strategic advantage.

When India imports these things and assembles them into a satellite branded "Made in India," the label is technically accurate and strategically misleading. The value, and the knowledge, remain elsewhere.

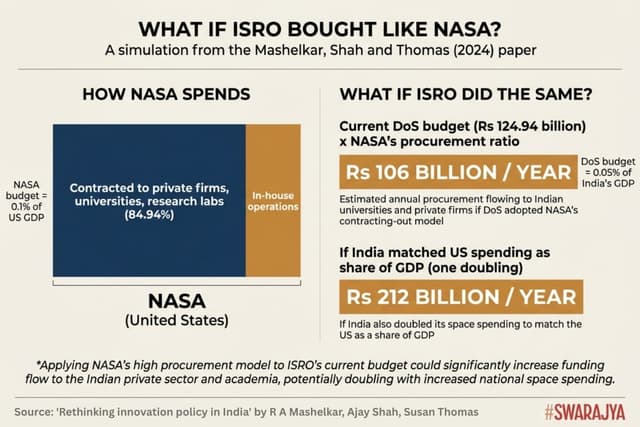

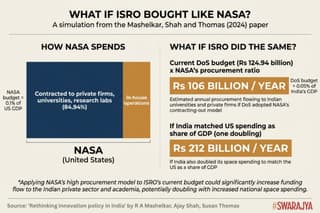

A 2024 paper that I really like comes to mind. The paper by R A Mashelkar (former Director General of the Council of Scientific and Industrial Research), Ajay Shah, and Susan Thomas documents a structural divergence between how NASA and ISRO spend their budgets.

NASA has contracted out between 75 and 85 per cent of its budget to external parties, including private firms, universities, and research labs, consistently since its founding in 1958.

ISRO, by contrast, is predominantly a "make" organisation: it designs, manufactures, tests, and operates most of its systems in-house. As a result, India's public space spending generates far fewer knowledge spillovers into the broader economy.

When NASA buys a component from a private firm, the firm retains the capability, trains engineers, develops adjacent technologies, and eventually sells to other customers in military, commercial, and international markets. The knowledge fans out. When ISRO makes the same component internally, the capability stays locked inside a government laboratory.

The paper calculates that if the Indian Department of Space organised its procurement the way NASA does, roughly Rs 106 billion per year (2024 estimates) would flow into India's universities and private firms. At present, most of that remains within ISRO, though the Covid-era opening up of the space sector to private companies is driving change in the desired direction.

At NASA's Jet Propulsion Laboratory (JPL), 90 per cent of components come from outside industry, the space-tech engineer tells this writer. JPL's job is to integrate. "Here," he observes, "everything is from ISRO only."

Why the Middle Is Missing

The reasons for this are structural, and they operate at multiple levels simultaneously.

The first, according to a space-tech company founder who did not want to be named, is the "VC problem".

India's VC ecosystem is believed to be configured more for software-style returns: invest early, scale fast, exit within seven to ten years through acquisition or IPO.

Hardware businesses, especially niche precision hardware businesses, do not fit this template. A company making space-grade optics might need five to seven years just to qualify its first product, followed by another three to five years to build a customer base. The addressable market is small. The unit economics are unfamiliar to investors trained on SaaS multiples.

Punit Badeka, co-founder of Eon Space Labs, pitched dozens of investors and was told, uniformly, that precision optics was too "niche" a market, that maybe a satellite company would acquire him someday.

The second is government procurement design. SBS-3, India's most consequential military space programme to date, illustrates the pattern.

The first phase of the Rs 27,000-crore programme was awarded to three firms: Dhruva Space, Pixxel, and Ananth Technologies. Dhruva and Pixxel are VC-funded startups that have built real design capabilities in-house; Ananth is a long-standing ISRO vendor that calls itself the largest contributor of subsystems to the Indian space programme.

For SBS-3, all three have taken on the satellite integration role, building complete spacecraft.

This is progress, and the contract does include a domestic content mandate: roughly half of the realisation of mission cost is to be sourced within India, according to one space-tech founder.

But the mandate runs into a ceiling. Key components like high-grade sensors and optics of certain specifications are simply not available domestically. The contract cannot enforce what the industrial base has not yet produced. The vendor has been promoted, but the component ecosystem beneath it has yet to be built up.

There is a real tension here. India faces an asset deficit of over 150 satellites against its principal adversary. Insisting on full domestic sourcing before the industrial base exists could slow the programme precisely when speed matters most. But building the satellites entirely, or even overwhelmingly, with imported subsystems locks in the dependency for another generation.

The question is whether the programme can do both simultaneously: deliver the constellation at pace while using a portion of the budget to deliberately cultivate the missing supply chain.

The alternative approach, the one the satellite engineer advocates, would be to identify the critical subsystem categories (gyroscopes, star trackers, reaction wheels, atomic clocks, optical payloads, onboard computers, ADCS units, propulsion modules) and place five-year development orders with two or three Indian firms in each. This is how NASA built Zygo, he contends. Not by waiting for the market but by creating it.

ISRO's Inertial Systems Unit (IISU) makes gyroscopes in-house, but they are less accurate than Western systems, and because ISRO never orders them externally, the technology stands to stagnate without competitive pressure.

Machines capable of achieving a λ/4 surface finish exist in India, but the λ/20 standard, the most precise level required for export-grade space optics, is not available in the private sector. The gap between λ/4 and λ/20 is the gap between serviceable and globally competitive.

More such machines need to be made available for the industry to capitalise on the export opportunity in precision optics. CSIR laboratories, which might conduct space-grade materials research, are not engaged in the space supply chain.

The institutional reflex is to keep everything inside. When Vannevar Bush designed the National Institutes of Health in 1945, he laid down an explicit principle: the agency "should not operate any laboratories of its own." India adopted the opposite model. ISRO kept the interesting problems. The repetitive production went to vendors who built to ISRO's specifications, not their own designs.

The third structural barrier lives in the fine print of government accounting rules, and it is worth distinguishing between the part that has recently been addressed and the part that has not.

In June 2025, the Ministry of Finance amended the General Financial Rules (GFR) to ease procurement for scientific institutions.

Purchase limits without quotation were doubled. Committee procurement ceilings were raised from Rs 10 lakh to Rs 25 lakh. GeM exemptions were introduced for scientific instruments. Vice-chancellors and directors of research institutions can now approve Global Tender Enquiries up to Rs 200 crore.

The reforms apply to the Department of Space, DRDO, and every major scientific ministry. They were welcomed across the research community as overdue, and they are genuine progress.

But buying equipment faster is not the same as contracting out research.

The deeper barriers remain intact. Rule 230 of the GFR still restricts government grants to educational institutions, cooperatives, and government bodies, excluding private for-profit firms.

Rule 225 still says cost-plus contracts should be "ordinarily avoided," the opposite of what early-stage research needs, where uncertainty is high and failure is to be expected.

There is no chapter on peer review. No framework exists for the kind of graduated contracting that NASA uses routinely: cost-plus at the concept stage, fixed-price at production.

As the 2024 paper's co-author, Ajay Shah, has put it, the procurement system remains "oriented towards buying pencils": if you fail to deliver pencils, you do not get paid or you get sued. That is fundamentally incompatible with risk-taking. And if it is not risk-taking, it is not research.

What is needed, Shah argues, are two new pathways in the GFR: grants and cost-plus contracts. A sophisticated society, he says, is one in which failure takes place without blame.

The June 2025 reforms made it easier for ISRO to buy, say, a spectrometer, but not to fund a private firm to develop an indigenous atomic clock.

The fourth barrier is human, and here, the most authoritative voice in India's space ecosystem has been characteristically blunt.

Former ISRO Chairman S Somanath, speaking at Accel's Advanced Manufacturing Summit in Bengaluru in August 2025, said that even ISRO, with decades of experience, "finds it difficult to find industrial partners with the required expertise in propulsion systems, precision tooling, as well as composite materials."

If you want to build a rocket engine in India, he noted, "you still have to rely on organisations like Godrej for manufacturing. But they can't put it all together themselves. The final assembly still comes back to ISRO."

The problem, Somanath argued, is not design capability. "We have good designers, but not enough people who understand manufacturing itself — tooling, processes, thermal design, or materials."

At the Global Investors Meet Invest Karnataka 2025 in February, he was sharper still: "When it comes to hardware, especially in aerospace structures, I am not seeing that type of competence or the capability to innovate or do things differently from the past."

This is India's former ISRO chairman, the man who oversaw Chandrayaan-3's lunar landing, saying that the proper manufacturing ecosystem does not exist even for ISRO's own needs.

His successor, V Narayanan, has said similar things from a different angle. At the National Aerospace Manufacturing Seminar in January 2025, Narayanan disclosed that India has been unable to produce a single semi-cryogenic engine successfully despite the project being approved 15 years ago, "due to the technological challenges" in manufacturing.

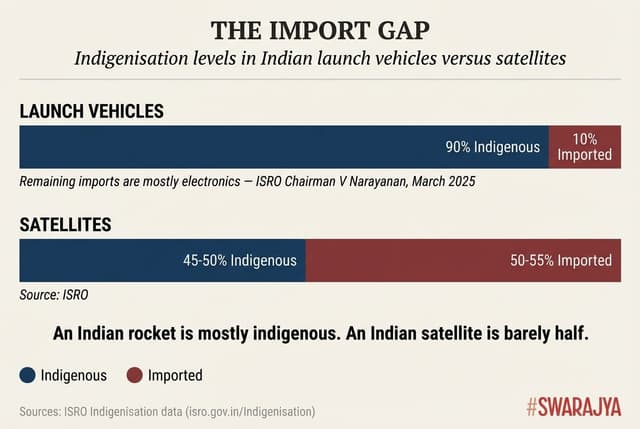

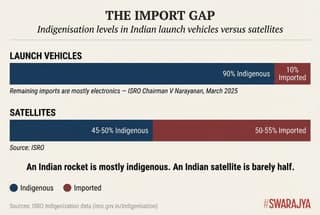

At a separate event, the Nano Electronics Roadshow at the Indian Institute of Science (IISc), Bengaluru, in March 2025, he noted 90 per cent of launch vehicle components are now indigenous, but the remaining 10 per cent, mostly electronics, are still imported.

For satellites, the picture is different: ISRO's own data puts the import component at 50 to 55 per cent.

Is it a talent problem? Giri puts in cultural terms: "Boring jobs earn you a lot of money. Kids today are not ready to do boring jobs. Everybody wants to have their share of attention."

The material scientist who can characterise a fused silica substrate, the precision machinist who can hold a 5-micron tolerance: these people do exist in India, but they are offered Rs 30,000 a month at startups that cannot pay better.

The deep-tech founder who has spent years in a PhD programme and a postdoctoral fellowship, who understands the science from first principles, is rare in a startup ecosystem dominated by engineers who can write software and build systems but have not done the grinding bench-level work required to push a material or a process beyond the state of the art.

The Case for Patience

Not so fast, some in the industry might say. There is a counterargument to the alarm, coming from a different theory of sequencing.

Prateep Basu, founder of SatSure, a company that operates at the intersection of space technology and artificial intelligence (AI), argues that component specialists can only thrive when successful "primes" generate enough domestic demand first.

The right order, in his view, is to build the Pixxels, Skyroots, and Dhruva Spaces into globally competitive satellite and launch companies, let them win contracts at home and abroad, and watch as the resulting volume creates the conditions for Indian subsystem makers to emerge.

Basu points out that the structural preconditions for component-level companies simply did not exist until recently. Before 2020, the only demand for space hardware came from ISRO's limited mission schedule and a small defence market. There was no support ecosystem for the academic researcher who might have a breakthrough in atomic clock design but had no idea how to manufacture it, qualify it for space, or raise capital to build a facility.

The ecosystem catalysis that IN-SPACe is now doing, bridging academic research and industrial innovation, has only started in the last few years. The government's Research, Development, and Innovation (RDI) funding is new but extremely promising. "It is a matter of time only that you will start hearing about more specific component-level research and companies," Basu says.

He also pushes back on the characterisation of vertical integration as glamour-seeking. In space hardware, the business is global. If an Indian company wants to compete with European or American satellite builders, offering a customer a full package (bus, payload, launch coordination, ground segment) is rational business strategy, not vanity.

In that light, Pixxel expanding from payloads to satellite platforms, Bellatrix moving from propulsion to orbital transfer vehicles: these are natural expansions of the addressable market from a core competency.

On SBS-3 specifically, Basu is optimistic about its potential to spur domestic innovation. "The number of satellite missions ISRO would do is very limited, and the scope for private sector involvement is also limited," he says. "Now with defence space demand also shaping up, such as for the SBS-3 kind of programmes, the cost of subsystems will have to be brought down by local innovation."

Great points, though there still remain some vulnerabilities in the equation. It is also worth noting, first, that ISRO and DRDO never cultivated a domestic component supply chain over decades of operation. Companies like Pixxel and Dhruva Space have built real design capabilities in-house, but expecting VC-funded startups to single-handedly correct for that institutional gap is unreasonable.

The first vulnerability is that the sequencing assumes Indian primes will eventually source domestically. They may not, not without deliberate intervention. Will a rational programme manager risk a Rs 100-crore satellite mission on an unproven Indian subsystem when flight-heritage French components are available off the shelf?

The first domestic order is always the riskiest, and no one wants to be first.

This is a classic market failure: the social benefit of creating an Indian atomic clock industry far exceeds the private benefit to any individual satellite builder of using an Indian atomic clock. Without a mechanism to bridge that gap (a government procurement mandate, a cost-plus development contract, a Zygo-style early order) the rational choice for every prime will be to import.

The second is the strategic vulnerability argument. Atomic clocks on India's NavIC navigation satellites, the first generation of which were all imported from the Swiss firm SpectraTime, now part of the French defence conglomerate Safran, have failed on five of eleven satellites launched.

ISRO has since begun flying indigenous atomic clocks, starting with NVS-01 in May 2023, and NVS-02 carries a combination of indigenous and imported clocks. But this was more of a forced correction born of a crisis than a planned capability-building exercise. Only four NavIC satellites are currently functional for positioning, navigation, and timing services.

One of those, IRNSS-1F, is operating on its final functioning clock. If that clock fails, NavIC drops below the minimum operational threshold and becomes, in the assessment of the ISRO watcher who goes by the name "SolidBoosters" on the social platform X and who uncovered the scale of these failures through RTI requests, "completely unusable".

ISRO has conducted a root cause analysis but refused to share it, calling it "vital technical information".

The failed clocks were all imported. Safran has this monopoly because India never nurtured a domestic capability. This is an active crisis in India's most strategically sensitive space system.

Similarly, if the US were to restrict export licences for, say, Ansys, the simulation software on which virtually all Indian aerospace engineering depends, India would be in what the satellite engineer calls "a pathetic state".

These are single points of failure in national capability, and the argument that the market will eventually solve them requires a level of faith.

The third vulnerability is especially telling, and it can be inferred from Basu's own experience.

SatSure built its satellite payload (optics, sensors, electronics) in-house over three years. It did so because geopolitical conflict demonstrated that access to commercial satellite imagery could be cut off at any time, creating what Basu calls "a business continuity problem."

He became his own component maker because no Indian component maker existed. That is not the market working as theorised. It is a workaround for the market's absence.

The Thin Middle

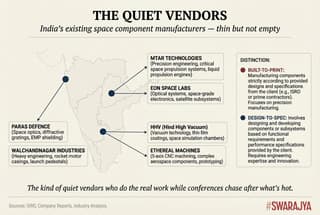

Sure, the middle is thin, but it's not empty.

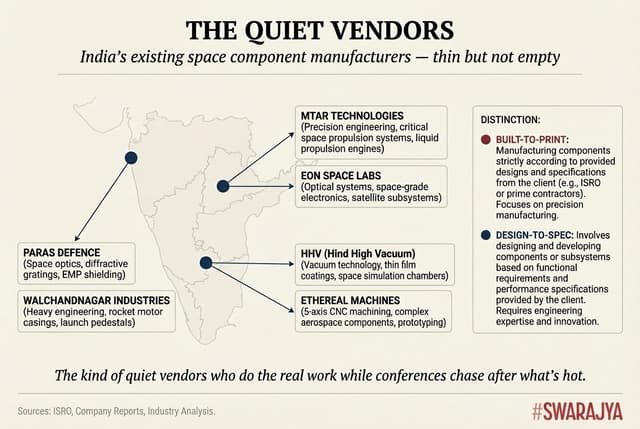

MTAR Technologies, headquartered in Hyderabad, was founded in 1970 by two engineers with four machines in a small workshop. The Department of Atomic Energy needed coolant channel assemblies for a nuclear reactor core. HMT, the state-owned machine tool company, said the job was too complex. The two founders, then employees at HMT, quit and took on the challenge.

Fifty-five years later, MTAR has 3,000 employees, seven manufacturing units, and supplies liquid propulsion engines, cryogenic engine assemblies, electro-pneumatic modules, ball screws, and actuator assemblies for ISRO's PSLV, GSLV, Chandrayaan, Mangalyaan, Aditya L-1, and Gaganyaan missions.

Their manufacturing tolerance is 5–10 microns. They have also never raised venture capital, never appeared on a magazine cover, and are virtually unknown outside the defence-industrial community despite being indispensable to every major Indian space mission of the last three decades.

MTAR is exactly the kind of company that Giri describes when he talks about the "10,000-odd quiet vendors" across Gujarat, Mumbai, Hyderabad, and Bengaluru who do the real work while conferences celebrate what is hot and buzzing.

HHV (Hind High Vacuum), based in Bengaluru, has 30 years of precision optics coating experience. Paras Defence, a listed company in Mumbai, does defence optics and heavy engineering. Walchandnagar Industries does heavy fabrication for ISRO.

These are not "startups". They are mature, quiet, precision-focused firms that have been doing this work for decades.

But they are not all equivalent. There is a meaningful distinction between "built-to-print" firms, companies like Ananth Technologies and Paras Defence that have mastered manufacturing to external specifications (Paras Defence's optics IP, for instance, is Elbit Systems', not its own), and "design-to-spec" firms like Centum Electronics and HHV that design, build, and manufacture with their own intellectual property. The latter category represents deeper strategic value.

India needs both, but the second category more accurately constitutes genuine indigenous capability.

And then there are the job shops (the plural "shops" may paint the wrong picture) that machine the mechanical components everyone needs.

Kaushik Mudda runs Ethereal Machines, a Bengaluru-based precision manufacturing company, and his order book is a map of the ecosystem's contradictions. "There is no space-tech startup in India that I have not done components for," he says. "I've done it for everyone over the last three years."

Done all these — housings, enclosures, structural parts, gimbals for electro-optic systems, manifolds, propulsion components, avionics enclosures, in Inconel, titanium, aluminium.

"But the volumes are very low. Given the number of launches is very low, it becomes not an area of focus," he says. The engineering effort required to make one precision component for a space startup is the same as for any other sector, but other sectors offer repeatable orders.

Mudda sees the ecosystem from a vantage point different from others voiced above: the view from the shop floor where metal actually gets cut. And what he sees is a structural disconnect. The legacy vendors (Ananth, Centum, MTAR) work with ISRO and DRDO because those orders are high-value and high-volume enough to justify the effort. "They usually shy away from working with any of these startups to that large an extent, but hopefully that will change soon," he says.

The startups, meanwhile, need components but cannot generate large enough orders to interest capable manufacturers. The result is that the existing manufacturing base and the new startup ecosystem are not connected.

His broader diagnosis cuts across sectors: "Even if you look at electronics, what is happening in India is mostly all assembly, which is an important step one. The actual manufacturing of it is not happening, which we need to move towards as a country."

Founders are gravitating towards simpler metal components (CNC parts, sheet metal) because those are at least feasible domestically. "But anything that comes from slightly higher up the value chain, everything is coming from outside," Mudda says.

Nobody wants to do the unglamorous work, he says, echoing Giri almost word for word. "No one wants to do boring work from what I know." And yet he is, in his own words, "a firm believer in building grounds-up": that if you perfect the individual components first, the end product follows, and the applications multiply.

A lens designed for satellite optics can, with further research, serve the semiconductor field. A precision housing machined for a space startup can serve defence, aviation, and medical devices. The component layer is where the spillovers live.

Then there is Eon Space Labs, the Hyderabad-based startup making precision optics for satellites and defence applications. It is one of the very few Indian companies attempting to manufacture, rather than import, the payload components that determine whether a satellite actually works once it reaches orbit.

Eon's co-founders, Sanjay Kumar, Punit Badeka, and Manoj Kumar Gaddam, have built germanium-free infrared lenses using chalcogenide and zinc sulphide that deliver better resolution at less weight, with a three-to-four-week lead time against six months and Rs 60–70 lakh for comparable imports from Israel, France, and Germany.

The team has achieved 80 per cent indigenisation and brought their rejection rate from 40 per cent down to 1 per cent. The startup has won an iDEX challenge and is in the fourth year of developing a multi-spectral handheld device for the Navy. Eon has a partnership with HHV, backed by a $1.2-million (approximately Rs 10-crore) investment from the MounTech Kavachh fund. The company has export orders lined up.

The Mira telescope has an origin story worth telling.

Badeka and his co-founders learnt that miniaturised telescope optics were being hand-polished abroad, a process that took three months per lens. Using their experience with ultra-precision diamond turning machines, Eon replicated the optic in seven days and sent it for independent validation. It met specifications. From that proof of concept, Eon moved to manufacturing in space-grade fused silica, the version that flew on PSLV C-62.

It is a small story, but it illustrates something important: the latent manufacturing capability exists in India. What is missing is the institutional architecture to scale it.

But Badeka will also tell you that λ/20, the most precise surface finish standard in space-grade optics, is not available on machines in the Indian private sector, that most startups import components and assemble them, then claim "Made in India".

That his own business model, staying an optics specialist, not becoming a satellite maker, is swimming against the current in an ecosystem that rewards integration over depth.

That startups face real difficulty arranging the matching contributions required by iDEX, and that it was only when a fund like MounTech Kavachh provided additional capital support that Eon could expedite the process from prototype to field trials.

On 12 January 2026, Eon's Mira telescope, a miniaturised instrument machined from space-grade fused silica, with 500-unit export orders already in the pipeline, was aboard PSLV C-62 when it lifted off from Sriharikota.

Eight minutes in, the rocket's third stage lost chamber pressure. The vehicle tumbled, and everything was lost. It was the second consecutive PSLV failure from the same third-stage anomaly. ISRO has stated that "the PSLV-C62 mission encountered an anomaly during end of the PS3 stage" and initiated a detailed analysis.

A national-level expert committee, chaired by former Principal Scientific Adviser K VijayRaghavan and co-chaired by former ISRO Chairman S Somanath, has since been constituted to examine what ISRO has described as systemic issues in the programme, including manufacturing processes and quality assurance.

Badeka and the team, meanwhile, are building another telescope.

Building the Middle

The prescriptions are less dramatic than the diagnosis might suggest.

Straight away, ISRO and DRDO could use the SBS-3 programme's Rs 27,000-crore budget as a lever: require the three satellite integrators to source a specified percentage of subsystems from Indian component manufacturers, with qualification timelines built into the contracts.

They could place blanket five-year development orders in critical subsystem categories, the way NASA created Zygo, Ball Aerospace, and Draper. They could open ISRO's test facilities to private firms systematically, not through ad hoc applications.

They could measure success not just in satellites launched but in subsystems exported, a metric that reveals whether India is building genuine capability or just assembling imported parts under an Indian flag.

Take solar panels as an illustration. The most critical testing and qualification facilities for space-grade solar panels remain largely inside ISRO. A private firm making panels has no way to independently qualify its product.

If ISRO were to order solar panels from two companies for five years, those firms would invest in their own testing equipment and supply panels qualified to TRL 7 or 8. ISRO would fly them, validate them in space, and then step back from the testing burden entirely. Eventually, satellite makers from other countries would come to India to get their panels tested.

The same logic applies to every critical subsystem category: gyroscopes, star trackers, reaction wheels, atomic clocks, optical payloads, onboard computers.

This kind of mindset, as the satellite engineer puts it, does not exist at present.

There is also a simpler lever that Mudda advocates: production-linked incentives (PLI) for the component layer, not just the OEM layer.

India's existing PLI schemes reward end-product manufacturers (there is a PLI for drone makers, for instance) but nothing trickles down to the firms making the components inside the drone.

"We need to start a PLI for the component manufacturer layer and not the OEM layer," Mudda argues. "That's how you tackle this problem and get founders to do the unglamorous, unsexy work."

Some of the broader architecture is already moving. The Union Budget for 2024-25 established a Rs 1 lakh crore corpus for interest-free loans to support research and innovation across sunrise domains including space and defence. The National Research Foundation Act of 2024 creates a framework for university-industry research.

IN-SPACe is beginning to recognise payload manufacturers, not just satellite builders. iDEX challenges are producing results. The direction is right. The question is whether the pace matches the vulnerability.

"People are just talking about the rockets," says Badeka, who is building his next telescope. "They are just talking about the satellites. But what is actually bringing an impact is these payloads."

The payloads, the components, the middle: here is where the next chapter of India's space story gets written, hopefully, in deep ink.

Karan Kamble writes on science and technology. He occasionally wears the hat of a video anchor for Swarajya's online video programmes.