Technology

India's LPG Crisis Has An Indigenous Fix. It's Been Waiting Since 2020.

Swarajya Staff

Mar 12, 2026, 01:04 PM | Updated Mar 14, 2026, 03:44 PM IST

When the Strait of Hormuz comes under threat, India's kitchen is one of the first things that feels it.

That is not an exaggeration. India consumes roughly 31.3 million metric tonnes of LPG a year and imports between 60 and 67 per cent of what it needs, depending on which source you consult. Over 90 per cent of those imports transit through the Strait.

When the current Iran-US-Israel conflict disrupted shipping through that chokepoint, the effects were almost immediate: weekly LPG imports fell by an estimated 30 per cent, commercial cylinder supply was halted in cities across the country, and the government invoked the Essential Commodities Act to prioritise household supply.

The short-term response has been broadly sensible. Refineries have been directed to maximise LPG output. Alternative supply from the United States, Australia and Algeria is being sourced. India had already signed a 2.2-million-tonne LPG supply deal with the US Gulf Coast; that diversification now looks prescient rather than merely prudent.

All good, but rerouting supply from one set of foreign sources to another does not solve the underlying problem. It manages it. And it introduces new complications: US LPG is propane-dominated (a byproduct of natural gas processing), while India's cooking-fuel requirement calls for a roughly 60:40 butane-to-propane mix. Middle Eastern LPG, produced as a byproduct of oil refining, happens to match this profile.

Diversifying away from the Gulf, in other words, is not just a matter of longer shipping times. The chemistry does not line up as neatly.

The structural problem is that 330 million Indian households cook on a fuel whose supply chain India does not control. For as long as that is true, a war, a mining operation, or even a diplomatic falling-out in West Asia can hold India's kitchens to ransom. Diversifying suppliers is useful. Diversifying fuel is even more critical.

The Technology on the Shelf

On 10 March 2026, Dr Raghunath Mashelkar, former Director General of CSIR, former Director of NCL, and former Chairman of the Scientific Advisory Committee to the Ministry of Petroleum and Natural Gas, posted a pointed message on X.

His argument was simple: India already has an indigenous cooking-fuel technology that can substitute for LPG. It is produced from Indian feedstocks, it burns cleaner, and the demonstration work is done. What it needs now is institutional support to scale up.

The technology Mashelkar is referring to is Dimethyl Ether, or DME.

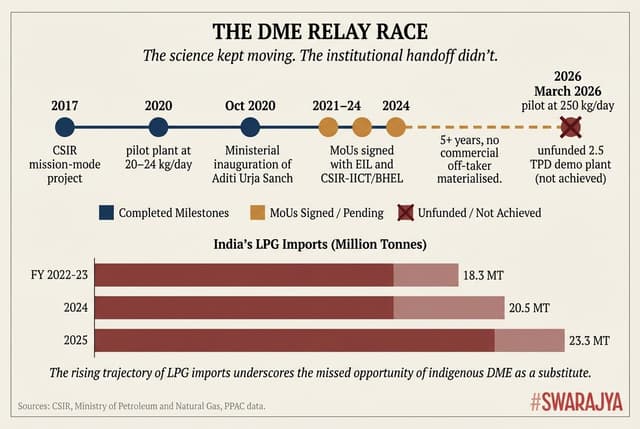

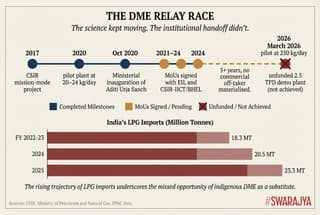

CSIR's National Chemical Laboratory (NCL) in Pune has been working on it since at least 2017, when CSIR approved a mission-mode project on catalysis for sustainable development.

The process is straightforward in concept: methanol is dehydrated in the presence of a catalyst to produce DME. India's own coal or biomass can serve as the feedstock for the upstream methanol synthesis, making the entire chain, from raw material to cooking fuel, producible domestically.

The chemistry is sound. DME is a gas at ambient conditions but liquefies under modest pressure, about 6 bar at 25 degrees Celsius, which gives it handling and storage properties similar to LPG.

It can be blended with LPG at up to 20 per cent without significant infrastructure changes; the Bureau of Indian Standards (BIS) has already notified a standard for this.

CSIR-NCL has also demonstrated a specially designed burner stove that can run on 100 per cent DME. The combustion is cleaner (lower NOx, lower SOx, no soot) and efficiency trials have shown 10-15 per cent improvement over conventional LPG burners.

CSIR-NCL's own technology one-pager, dated February 2020, describes the process parameters: selectivity above 98 per cent and conversion above 84 per cent at 10 bar, with a novel metal oxide catalyst and an in-situ product purification design.

At the time, the pilot plant operated at 20-24 litres per day. Since then, the technology has been scaled up to 250 kg/day. According to Mashelkar's post, partners are ready to build a 2.5-tonne-per-day demonstration plant quickly, and he is urging the Centre for High Technology (CHT), the Ministry of Petroleum's dedicated technology body, which has the funds and the mandate for exactly this kind of project, to move on it.

CSIR-NCL is not working alone, either. Engineers India Limited has signed an MoU with CSIR-NCL for the development and commercialisation of DME technologies.

Separately, CSIR-IICT in Hyderabad and BHEL Corporate R&D have signed an MoU under DST's Carbon Capture and Utilisation initiative to develop a CO₂-to-DME pathway, converting captured carbon dioxide directly into DME through catalytic conversion. This would offer a cleaner production route entirely, one that skips the coal gasification step and addresses the emissions concern head-on.

In May 2025, at a CSIR-NEERI workshop on clean energy, IIT Jodhpur Director Prof Avinash Kumar Agarwal called methanol and DME "low-hanging fruits" for India and urged scientists to prioritise them.

The interest is not limited to government labs. In December 2025, Godavari Bio-refineries Limited — a listed Somaiya group company and one of India's largest integrated bio-refineries — launched a pilot to convert industrial CO₂ directly into DME, in partnership with the Institute of Chemical Technology (ICT), Mumbai.

That a private-sector player with ethanol supply chain experience is investing its own capital in DME is exactly the kind of commercial signal the technology has been waiting for.

The Honest Accounting

A 2.5 TPD demonstration plant will not suffice to counter the current LPG crisis. India's daily LPG demand runs to about 85,000 tonnes. The gap between where the technology sits today and where it would need to be to materially reduce import dependence is four orders of magnitude. DME is, therefore, not a short-term answer to the Hormuz disruption.

Here we can heed Mashelkar. His post is a call to use the urgency of the present crisis to do something that should have been done years ago: commit seriously to scaling a technology that is otherwise ready. The crisis is the catalyst, not the use-case.

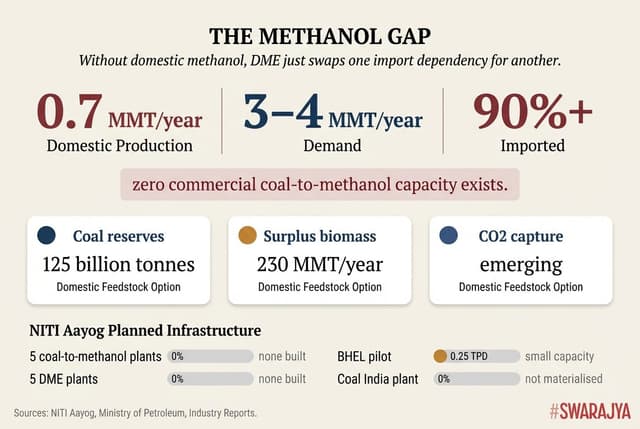

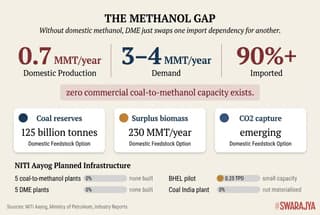

There is also a feedstock question that deserves honest attention. The feedstock for DME is methanol. And here is the catch: India currently imports over 90 per cent of its methanol.

Domestic production stands at roughly 0.7 million metric tonnes against demand of 3-4 million tonnes. Every existing Indian methanol plant runs on natural gas or naphtha, both of which are themselves imported.

So a DME programme that simply uses today's methanol supply would, in effect, be substituting one import dependency for another, swapping LPG from West Asia for methanol feedstock from elsewhere. That does not solve the structural problem. The whole point of DME is that India has the raw materials to produce its own methanol.

Coal-to-methanol-to-DME is the proven pathway. China has built it at enormous scale: about two-thirds of Chinese methanol comes from coal, and the country has had DME production capacity exceeding 10 million tonnes per year, with most of it going into LPG blending.

India has vast reserves of high-ash coal, which makes it an available feedstock. But a national cooking-fuel programme running on coal gasification would sit uneasily with India's climate commitments.

The cleaner path runs through biomass: India generates approximately 230 million metric tonnes of surplus agricultural biomass annually, plus around 62 million tonnes of municipal solid waste. Biomass-to-methanol-to-DME is technically feasible, though it requires more development at scale than the coal route.

The CO2-to-DME pathway being developed by CSIR-IICT and BHEL opens a third option. A serious DME programme would need to specify which feedstock pathway it is pursuing and at what pace, and be transparent about the trade-offs.

There is a cautionary note here from abroad. Indonesia, which faces a similar LPG import dependency, has been trying to build coal-to-DME capacity. A recent analysis by the Institute for Energy Economics and Financial Analysis found the economics hard to justify: a 1.4-million-tonne DME plant would cost USD 2.6 billion in capital expenditure alone, and consumers would pay 42 per cent more per unit of energy than LPG.

In China, Shanxi Lanhua halted DME production in 2023 due to unprofitability. The lesson is not that DME is unviable, but that scaling it requires getting the economics right from the start, especially the feedstock pathway.

From 2020 to Now: What Moved and What Didn't

The current crisis has brought DME back into the conversation. But the technology's prior moment in the spotlight tells a more instructive story.

In October 2020, then-Science Minister Dr Harsh Vardhan virtually inaugurated CSIR-NCL's DME-fired Aditi Urja Sanch cooking unit, with DME-LPG blended cylinders handed to the CSIR-NCL canteen for trial. The occasion was attended by the DG of CSIR, the Director of NCL, and several senior scientists. It was presented as a step towards commercialisation.

To be fair, the technology has not stood still since then. The pilot capacity has grown roughly tenfold, from 20-24 litres per day in 2020 to 250 kg/day now. A contract manufacturer for the catalyst has been identified. An MoU with Engineers India Limited has been signed. These are real steps.

But the next leap, to the 2.5 TPD demonstration plant that was discussed then, has not happened. No commercial off-taker materialised. In the interim, India has continued to import roughly 20-23 million tonnes of LPG annually, almost entirely from West Asian suppliers, with near-total exposure to Hormuz disruptions.

It is also worth noting that the broader methanol economy, without which DME has no reliable feedstock at scale, is yet to take off. NITI Aayog has for years announced plans to build five coal-to-methanol plants, five DME plants, and a 20-million-tonne-per-year natural gas-based methanol facility in collaboration with Israel. These have yet to be built.

BHEL has a pilot coal-to-methanol unit in Hyderabad producing 0.25 tonnes per day. Coal India has planned a 0.7-million-tonne-per-year plant in West Bengal that has not materialised.

What Urgent Action Actually Means

Hopefully Mashelkar's immediate ask, CHT funding for a 2.5 TPD demonstration plant, is heeded, and quickly. But the medium-term programme that has to follow is more demanding than a single funding decision. It has at least three components.

First, India needs a methanol economy policy that actually creates domestic production capacity. The government has gestured towards a methanol economy for years, but without building the coal-to-methanol or biomass-to-methanol infrastructure that would give DME a reliable feedstock supply at scale.

This requires decisions about which feedstock pathway to prioritise, what the environmental guardrails look like, and how to structure the capital investment. Without domestic methanol, DME remains an import-dependent technology, and the entire point of the exercise is defeated.

Second, a DME blending mandate, analogous to the ethanol blending programme for petrol, would create the market signal that attracts commercial investment. The ethanol blending programme worked because it created guaranteed demand. A mandate requiring, say, 10 per cent DME content in LPG by a target date, conditional on domestic production ramping up, would do the same. BIS has already notified the standard for 20 per cent DME blending in LPG; the regulatory foundation exists. Without that demand signal, the economics for private investors remain uncertain.

Third, the cylinder and stove infrastructure needs attention. A 20 per cent DME blend in existing cylinders and stoves requires modest modification, but a higher-percentage or standalone DME programme requires redesigned equipment. The scale of India's LPG distribution network, 330 million households and multiple PSU distributors, means infrastructure transitions take years to execute. That planning needs to start now if the vision is anything beyond a demonstration plant.

The Larger Point

India's LPG crisis is a periodic reminder of a structural vulnerability. The good thing is that an indigenous alternative exists, developed by Indian scientists, demonstrated at Indian labs, rooted in Indian feedstocks. DME's potential has been on the record since at least 2017.

The science has kept moving: the pilot has scaled tenfold, the catalyst is ready for commercial manufacture, the MoUs are in place, and a cleaner CO2-based production route is now being developed alongside the original coal/biomass pathway.

The building blocks are there. India has the science, the feedstock, and now the urgency. What it needs is the institutional will to get going in this critical direction.