In January 2014, Tata Motors unveiled what it called India’s first indigenous turbocharged petrol engine. The Revotron 1.2-litre, fitted to the Zest sedan, was presented as a milestone — proof that Indian engineers could design a modern powertrain from a blank sheet.

The marketing was exuberant. The engineering reality was more complicated. AVL of Austria had optimised the design. Bosch of Germany supplied the engine control unit and calibration. Honeywell of the United States designed the turbocharger. Testing was conducted in the UK and South Korea. Tata owned the architecture and the intellectual property. But the word “indigenous,” in this context, was doing a lot of heavy lifting.

The Revotron story is not an indictment of Tata. It is a parable for India’s entire passenger car industry. After more than seven decades of automobile manufacturing, the world’s third-largest car market has never fully designed and built a passenger car engine without significant foreign engineering involvement. Almost every engine in every Indian car — past and present — traces its intellectual lineage to Europe, Japan, or the United States. This is not a matter of manufacturing capability. India builds engines at enormous scale and impressive quality.

It is a matter of design sovereignty — the ability to conceive, engineer, validate, and iterate a powertrain from first principles. Its absence helps explain why the country captures barely three per cent of global auto component trade despite being one of the world’s largest vehicle producers.

The archaeology of dependence

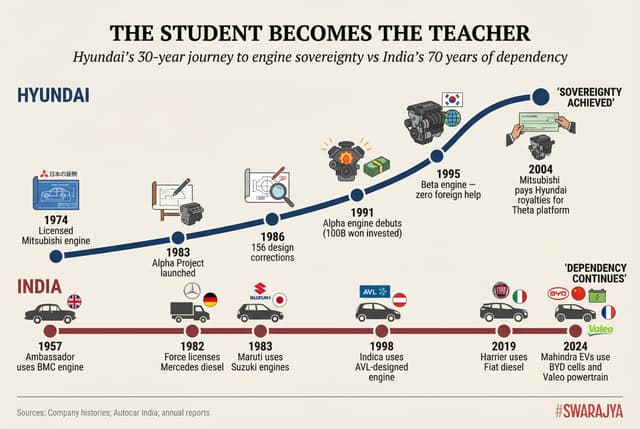

India’s automotive history is, at its foundations, a history of licensing agreements. Hindustan Motors produced the Ambassador from 1957 to 2014 using first a BMC B-Series engine from Britain, then an Isuzu unit from Japan. It never designed its own. Premier Automobiles built the Padmini with a Fiat engine whose lineage traced to a 1937 Italian design. Standard Motors of Chennai assembled vehicles with a Standard-Triumph engine from Coventry. Force Motors licensed the Mercedes-Benz OM616 diesel in 1982 and has built its entire range around that German architecture ever since. For the first four decades of Indian car manufacturing, not a single passenger car engine was designed on Indian soil.

India’s protected market, sealed behind tariff walls until 1991, should in theory have created space for indigenous development. In practice, it did the opposite. Protection guaranteed profits from licensed products, eliminating the competitive pressure to invest in original engineering. Maruti Suzuki, India’s largest carmaker with over forty per cent market share, has never designed a single engine in more than four decades. Every powerplant is designed by Suzuki Motor Corporation in Hamamatsu and manufactured in India.

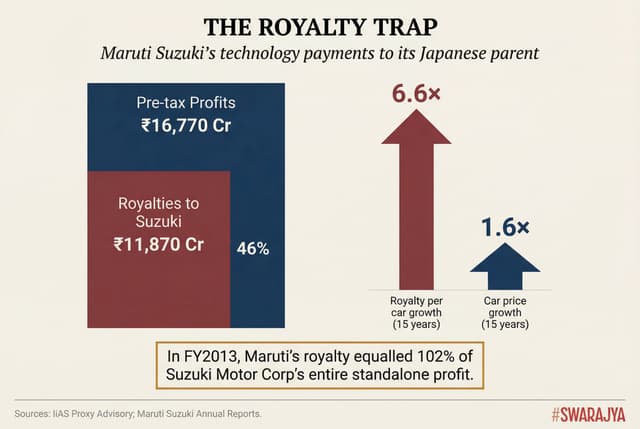

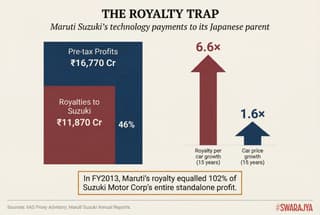

Over the five years to FY2015, Maruti paid roughly ₹11,870 crore in royalties to Suzuki against pre-tax profits of ₹16,770 crore — meaning up to 46 per cent of earnings were remitted to its parent as payment for technology the Indian company was never permitted to develop itself. Per-car royalty payments grew 6.6 times over fifteen years while average vehicle prices increased only 1.6 times. The proxy advisory firm IiAS described these payouts as “extortive,” noting that Suzuki’s own global R&D spending averaged four per cent of sales while it extracted six per cent from Maruti as royalty.

In FY2013, Maruti’s royalty payments equalled 102 per cent of Suzuki Motor Corporation’s standalone profit. The Indian subsidiary was, in effect, funding its parent’s entire operation. This is not a story about exploitation alone. It is a story about choices not made — about an industrial establishment that found it more convenient to rent technology than to build it.

Tata and Mahindra: half-steps toward sovereignty

Two companies have attempted to break the pattern. Tata’s Indica, launched in 1998, and the Nano’s 624cc engine, designed from scratch with 68 patents, demonstrated that Indian engineers could create original powertrain architectures. But Tata’s flagship SUVs, the Harrier and Safari, still run on a Fiat 2.0-litre Multijet II diesel produced at a Tata-Stellantis joint venture plant. Until late FY2025, any recalibration of the engine control unit required going through Stellantis at a reported cost of approximately €10 million per change. Tata brands this engine “Kryotec.” Its core intellectual property belongs to Italy.

Mahindra & Mahindra followed a more deliberate trajectory. It licensed Peugeot’s diesel engine in 1979 and manufactured it for 26 years — the “DP” suffix on models like the CJ540DP stood for “Diesel Peugeot.” When BS3 norms rendered the Peugeot non-compliant in 2005, Mahindra was forced into indigenous development, producing the mHawk 2.2-litre diesel with AVL Austria. Mahindra’s journey from 50 R&D engineers in a two-storey building at Nashik in 1993 to the 125-acre Mahindra Research Valley in Chennai illustrates that capability-building is possible. But even here, a critical distinction must be drawn about what “co-development” actually means.

The AVL question: who is really designing the engine?

AVL List GmbH is the world’s largest independent powertrain consultancy, with 12,200 employees and roughly €2 billion in revenue. Nearly every automaker uses AVL. But the nature of that engagement differs so profoundly between Indian and global automakers that it amounts to a difference in kind.

For BMW, Volkswagen, and Hyundai, AVL provides the last twenty to thirty per cent of the development process — simulation software, test-bed equipment, calibration support. BMW designs and manufactures all engines in-house; its Steyr plant employs 4,700 people producing over one million engines annually. When Volkswagen uses AVL, it purchases diagnostic modules. Hyundai licenses simulation software. These companies set the direction, define the combustion system, and do the fundamental engineering themselves. AVL polishes the last mile.

For Indian automakers, the relationship is inverted. AVL provides the first eighty per cent. Tata’s own annual report describes the Revotron — which powers its entire small car range — as an engine whose “design was optimised by AVL Austria,” with AVL named as “the lead global engine consultant.” The Mahindra Museum describes the mHawk as an engine “Mahindra, along with help of engine design house AVL, co-developed.” R. Velusamy, Mahindra’s head of automotive product development, told Autocar India of the mStallion: “It’s a highly complex and precise job and needs deep expertise; which our partners AVL provide.” AVL India’s managing director has stated that “AVL will handle engineering of the powertrain and hybrid systems” for Mahindra’s future vehicles.

The distinction matters enormously. Using a consultancy to validate your own design is standard practice. Outsourcing the architecture and fundamental engineering direction because your organisation lacks the institutional depth is something quite different. It means the knowledge stays in Graz, not Pune. It means the next engine will require another AVL contract, because the capability was never internalised. Each project builds AVL’s expertise, not the Indian OEM’s.

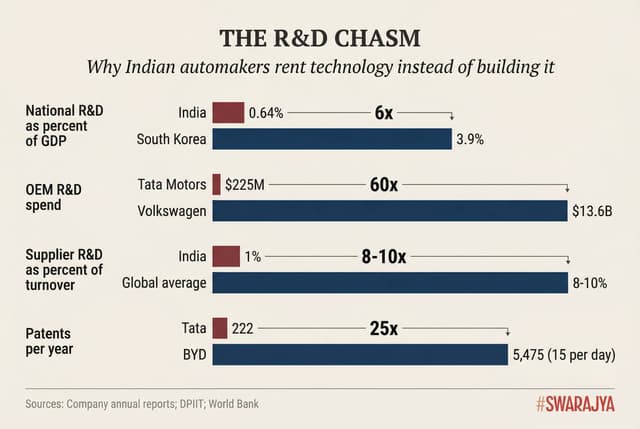

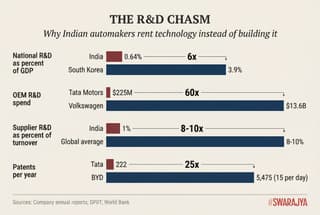

There is no accumulation of institutional knowledge, no cadre of engineers who did it once and can do it better the next time, no design culture that sharpens with each generation. The absolute R&D spending gap explains why: Tata Motors’ standalone Indian operations spend roughly $350 million on R&D annually. Volkswagen spends sixty times that. National R&D expenditure in India stands at 0.64 per cent of GDP, with private industry contributing just 0.3 per cent. South Korea spends 3.9 per cent. The gap is not a bug. It is the system.

What Korea did differently

Hyundai used licensed Mitsubishi engines from 1974 to 1991. In 1983, engineer Lee Hyun-soon launched the Alpha Project to design Korea’s first indigenous engine. Mitsubishi’s chairman reportedly dismissed the attempt as doomed. Opposition within Hyundai itself was fierce; executives and even Korean government officials preferred continued Mitsubishi dependency. After 156 design corrections in 1986 alone, testing in Arizona deserts and Canadian winters, and roughly 100 billion won in investment over seven years, the Alpha debuted in 1991. By 1995, the Beta engine was designed entirely without foreign consultancy. By 2004, in a reversal that deserves to be studied in every Indian boardroom, Mitsubishi was paying royalties to Hyundai for the Theta engine platform. The student had become the teacher in barely two decades.

Toyota’s first engine in 1934 was a direct copy of a Chevrolet inline-six. Within twenty years, it was designing fully original engines. Honda, uniquely, never used a single foreign engine design from its first car in 1963, reflecting founder Soichiro Honda’s identity as an engine man before he was a car man. China compressed the timeline further — Chery launched the ACTECO engine with AVL in just two years. Today, in a technology-flow reversal that would have seemed fantastical a decade ago, Geely supplies powertrains to Renault, Nissan, and Mitsubishi through their “Horse” joint venture. The common thread: foreign assistance served as a time-limited bridge, not a destination. India’s Tata and Mahindra have started this journey. Neither has reached the stage where a former technology supplier pays them royalties.

A supply chain that assembles — and an academy that is ignored

The dependency extends below the OEM level. Indian auto component suppliers invest approximately one per cent of turnover in R&D; global suppliers invest eight to ten per cent. ACMA’s president has acknowledged that India has generally been a “build-to-print” environment — executing someone else’s designs. There is no systematic supplier development programme — no design-led capability building, no leveraging of academia to bring subject matter expertise to mid-career professionals, no structured effort to upgrade the institutional knowledge base of the companies that make up the supply chain.

The handholding that Toyota and Hyundai did with their suppliers for decades — embedding engineers, sharing design methodology, co-investing in R&D — has no Indian equivalent. China’s auto component exports in overlapping categories are 5.6 times India’s.

Toyota’s keiretsu system cultivated suppliers that became engineering powerhouses — Denso, spun out in 1949, is now the world’s second-largest parts supplier with $49 billion in revenue, developing proprietary “blackbox parts” whose IP it owns. Toyota’s highest-tier suppliers embed guest engineers inside Toyota for multi-year rotations. Hyundai Mobis collaborates with 23 companies to build a domestic semiconductor ecosystem. When Toyota partnered with ACMA to train Indian suppliers, it was a foreign automaker building capability that Indian OEMs had not built themselves.

The academic dimension is equally stark. Toyota’s Research Institute has invested over $100 million across 21 American universities, generating 1,250 paper submissions and 69 patents. Hyundai’s Joint Battery Research Center at Seoul National University runs 22 projects in solid-state batteries. CATL invested $450 million in its 21C Lab with deep university collaborations. BYD employs 110,000 R&D staff and files roughly fifteen patents per working day.

Against this, Tata Motors has a five-year MoU with IIT BHU. No Indian automaker has established a dedicated, well-funded joint battery research centre at any IIT. No Indian automaker has funded endowed chairs in combustion science or battery chemistry. Tata Motors files 222 patents per year. BYD files 5,475. This is not a gap that can be closed with press releases.

From engines to batteries: the dependency recurs

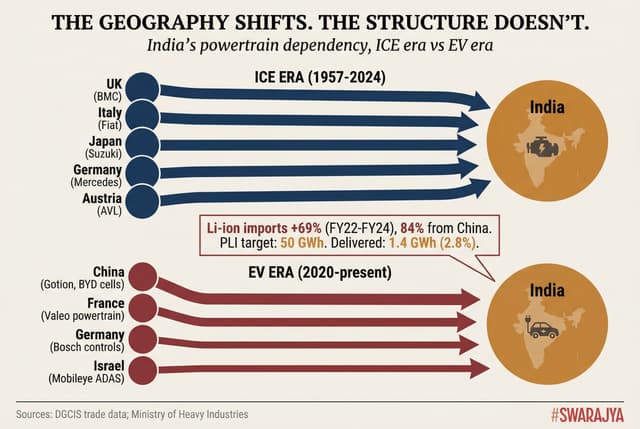

The electric vehicle transition was supposed to offer a clean break. The early evidence is troubling. Mahindra’s flagship INGLO platform was originally designed around Volkswagen’s MEB electric drive system — covering motors, battery modules, and cells for five SUVs targeting over one million units. When VW failed to deliver components on time, citing IP and compliance delays, Mahindra pivoted. The BE 6 and XEV 9e now use BYD Blade cells, a Valeo three-in-one powertrain integrating motor, inverter, and transmission, Bosch vehicle control, and Mobileye ADAS.

What Mahindra does engineer in-house — the platform architecture, battery pack assembly, thermal management, BMS, and software — is meaningful integration work. But it is not propulsion science. Mahindra’s contribution to the core EV powertrain — the parts that actually make the car move — is zero. At its two-hour launch event in November 2024, the company made no reference to Volkswagen.

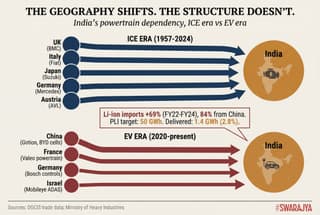

The contrast with BYD, where 75 per cent of components are manufactured in-house, or Hyundai, which designs its own 800-volt motors and holds patents on its multi-charging architecture, is devastating. Tata’s EVs source cells from Gotion High-Tech of China. Lithium-ion battery imports surged 69 per cent between FY2022 and FY2024, with over 84 per cent from China. The government’s PLI scheme to build 50 GWh of domestic cell capacity has commissioned just 1.4 GWh — 2.8 per cent of the target. The geography of dependency has shifted eastward. The structure is unchanged.

A commercial vehicle footnote — and a question

In commercial vehicles, where India-specific conditions demanded local solutions, companies have invested more. Ashok Leyland’s Neptune was a clean-sheet design; Tata’s Cummins joint venture now manufactures hydrogen engines. But even here, foreign engineering DNA runs deep.

The question is not whether India can manufacture at scale — it manifestly can — but whether it can innovate at the frontier. Maruti’s forty-year record of zero indigenous engines, Tata’s Italian diesels, Mahindra’s INGLO vehicles powered entirely by foreign components, a supplier base at one per cent R&D intensity, and IITs whose talent flows to Bangalore’s software parks rather than Pune’s powertrain labs — these are not failures of talent. Indian engineers lead R&D teams at virtually every major global automaker. They are failures of institutional ambition, of capital allocation, and of a policy environment that rewarded assembly over invention.

The EV transition compresses the available timeline brutally. China built its battery dominance over twenty years of sustained government investment, backed by tens of billions of dollars in subsidies and strategic acquisition of raw material supplies across three continents. India’s PLI scheme is a fraction of that scale, and the execution gap is alarming.

The industry generated $118 billion in revenue in FY2024. Whether it remains a high-volume, low-value manufacturing base — assembling foreign technology profitably but without strategic depth — or develops the engineering sovereignty to compete globally on innovation, depends on choices being made right now.

The history of the engine India never built is, ultimately, a history of choices not made. The EV era offers one more chance. The early signs suggest it may be learning this lesson too slowly.

(With inputs from CV Krishnan)

A public policy consultant and student of economics.